London’s Homebuilding Crisis: Putting Things in Perspective

4) Perspective Taking

It’s important to bear in mind that large-scale private new-build development in London is a relatively recent phenomenon. According to a comprehensive database assembled by the think tank Centre for Cities, between 1955 and 1975, only around 200,000 homes were privately built in the capital, around three-quarters in Outer London boroughs, just 5.4% of the nation’s total.

To put this in context, this is slightly less than what was built in the eight-year period between 2016 and 2023 (when delivery was more evenly split between Inner and Outer London), when the capital accounted for 14.9% of private delivery.

This is, of course, private development. Social and affordable housing was a different matter. Between 1955 and 1975, London built some 300,000 affordable homes, half as many again as the private sector, or 12.4% of the UK total.

Inner London’s record is even more stark: 126,207 affordable homes and just 41,238 private homes.

Indeed, between 1974 and 1984, some 63% of all privately built London homes were delivered in just 10 boroughs: Bromley, Sutton, Barnet, Hillingdon, Bexley, Havering, Richmond, Enfield, Kingston and Harrow. Presumably, this reflects family housing on (relatively) greenfield sites.

Some London boroughs that are now deeply desirable saw extremely low delivery over that period – Tower Hamlets (just 316), Hammersmith & Fulham (just 369), Camden (just 442), and Lambeth (just 489). Hackney, Greenwich, Brent, Islington, and Wandsworth all saw fewer than 1,000 (or fewer than 100 homes per year).

This was not a period of any urban private housebuilding at scale. The industry largely built suburban homes and the odd medium-rise block of flats, while urban development was largely the province of councils. The exceptions were a few infill schemes carried out in the more affluent parts of London. In other words, there was no real at-scale urban private housing model. (The big regional cities were no different, incidentally, although many lacked infill projects too).

The following ten years – between 1985 and 1994 – were not so different. Inner London boroughs were delivering somewhat more (typically 500-1,250), but the likes of Hillingdon, Bromley, and Enfield remained the standout deliverers. There were two exceptions: Southwark and Tower Hamlets, which saw almost 10,000 and almost 6,000 private homes, respectively. This was a sign of what was to come, as it reflects the first large-scale private residential development in London since the likes of Dolphin Square before the war – the regeneration of Docklands and parts of the South Bank and Surrey Docks respectively.

The modern era of London development, though, can probably be dated back to the likes of the Montevetro scheme in Wandsworth, which was completed in 2000. It was the first large-scale luxury flatted development outside Docklands and would set the scene for a new wave of private development in London. By 1995-2015, the league table of delivery was led by Tower Hamlets and Southwark, with Westminster and Wandsworth high up in the table, a position that would continue: Inner London boroughs had become major contributors.

This was, of course, a reflection of changing attitudes towards Inner London – a so-called ‘gentrification’ that was being matched by a reversal in prices (Outer London boroughs were largely more expensive than inner ones in the decades after the war).

The history can be seen clearly in the chart below – London providing 14-18% of new builds post-war (a combination of reconstruction in Inner London and, more importantly, suburban expansion that had been approved before the modern planning system was introduced in 1947), followed by London making a 4-6% contribution to total private housebuilding in the sixties, seventies and eighties, mostly accounted for by Outer London (Inner London providing less than 2% for much of this period).

But as London’s renaissance kicked in, the figures for both rose, with Inner London in particular seeing private development of residential that had not occurred at anything like that scale for a very long time – arguably since late Victorian times.

The ‘broken model’ issue is more of a concern for Inner London. Of the 2,153 starts in London over the first six months of 2025, only 23% were in Inner London. This compares with a long-term trend of 39%. The boroughs seeing the highest number of starts in London were Barking & Dagenham, Barnet and Hounslow, where values are lower, development is less dense, easier and comprises low-rise flats or townhouses, and there is less affordability stress.

A further problem is that affordable housing delivery is now more linked to private development in a way that it was not the case in the immediate post-war period – partly because of section 106 agreements, partly because of the nature of development in London, with a majority of flatted, mixed-tenure blocks that cannot be built piecemeal.

In the mid-1970s, around 15% of affordable housing in the UK was being delivered in London; by the 2010s, this had risen to as much as a quarter. As a result of the general problems and the link with the viability of private schemes, it was probably around 2% over the year to the end of Q2 2025.

This leads to two important conclusions. Firstly, that London’s private sector has become far more important to national housing delivery. Secondly, as social housing has also become linked to that same private sector, it has become linked to market cycles and more vulnerable to downturns, like this one, that disproportionately impact private development in London. This implies that there is a need for a rethink of the whole system, rather than just some – admittedly helpful – emergency measures.

London’s Homebuilding Crisis: Why Has Building in London Stalled?

3) Challenges

It is no exaggeration to say that London housebuilding has collapsed over the past year or so, leaving the industry in a state close to an emergency.

Over the past five years, the capital has delivered on average 38,220 new units. But according to the London residential development specialist research house Molior, construction began on 3,248 homes during the first nine months of 2025 – equivalent to an annual rate of 4,331. That is not only just 11% of what is needed to sustain the activity of the past five years, it’s also under 5% of the government’s target.

This is starting to filter into construction volumes and completions, which are now lower than at any point since the aftermath of the Global Financial Crisis. Molior estimates – presumably based on the lead-in times for new homes – that just 9,100 homes will complete during the entire 24-month period spanning 2027 and 2028: just 5.2% of the government’s target for London.

This emergency is of national importance. London is expected to deliver about 25% of the UK’s total housing over the next five years. And while other regions are down on longer-term trends, at 25% or so below, their problems are nothing like London’s. Far more properties are delivered as houses or low-rise flats, meaning building safety issues are marginal, while affordability is less stretched. But as London remains the most productive part of the UK economy, allowing low housing supply here, at a time when the government is desperately searching for higher economic growth, is deeply unwise.

There are other reasons why this building crisis qualifies as an emergency. The most glaring is that in London, homes will be more expensive and scarcer than they would otherwise have been. Even more worryingly, this crisis extends just as much to affordable housing delivery. This shares some of the same problems as the private sector, with the additional problem that grant funding is no longer sufficient to make schemes work. Affordable housing outside London does not face quite the same issues and is acting in a more countercyclical way, as the chart below shows.

With building activity at such low levels, there are risks of widespread layoffs in the construction industry and business failures, which could cause economic scarring. It will be difficult for the supply chain to bounce back quickly if conditions remain so dire; if things do not improve quickly, it could take years to rebuild capacity.

But why has building in London stalled?

There is no shortage of potential reasons for why housing delivery in the capital is struggling so much.

1) Viability is severely challenged:

Construction costs for new housing have risen dramatically since the pandemic, by 14% and 34% over the past three and five years respectively, according to government data. This may be an underestimate for higher-density homes.

This is partly a result of inflation in materials and labour costs, and partly a result of more expensive building regulations and requirements.

- This is compounded by the fact that competition among contractors – particularly for complex high-rise blocks – has reduced. This has allowed them to become more conservative, and given recent inflation, they appear to be building more headroom into estimates and prices.

- This means that the calculations of land value and viability made before this surge are now out of date. This is likely to be more marked for the flatted development that dominates delivery in the capital, as construction costs will account for a higher proportion of Gross Development Value (GDV). Flats also have more upfront costs, as they all have to be built at once – unlike houses, which can be ‘drip-fed’.

Debt costs for developers have also increased by as much as five percentage points. This adds further to costs.

2) Market activity has weakened

Weak off-plan demand. Overseas buyers – who used to underwrite the early stages of large schemes through pre-sales – have stepped back from London’s market. This is partly a reflection of Brexit, Covid and the UK’s economic difficulties, but is also a result of the government introducing measures, such as the SDLT surcharge in 2021, which discourage foreign investment. There are also more locations competing for their attention. Together with the ending of non-dom status, this also gives the impression that they are not welcome, and other measures may be incoming. Domestic investors are also dissuaded by other factors, such as changing tenant legislation. Many developers used to sell a significant chunk of their scheme off-plan to access finance and kickstart the scheme.

Effective demand from first-time buyers has also weakened. Mortgage costs have risen steeply, particularly for those buying with small deposits – many of whom will be first-time buyers. Put simply, with mortgage rates at 4-5%, a buyer on a given income can simply afford rather less than when they were at 1-2%. Sales rates per annum have fallen from a high of over 25,000 in 2015 to 11,650 in 2024 and are on track for a similar figure this year. But this might be misleading, as it could be limited by availability.

The fact that unsold stock is building up suggests that this is not the case, though. There are currently 3,678 unsold completed homes available in London – the second highest on record after 2019’s 3,767, although this followed several years when there had been 22,000-24,000 completions, compared to last year’s c. 16,000. The ratio of unsold homes to the previous year’s completions might be a better way to look at market tightness. Using this measure, around 23% of last year’s delivery total remains unsold, marginally down from the 25% recorded at the end of 2024 but well ahead of the 10-year average of 13%. The chart below gives the data in detail.

Another measure involves looking at how sales over the year compare to the same year’s completions. At the moment, that figure is 54%; last year it was 72%; the average is 97%. The extent to which total sales over the period exceed unsold stock is also a measure of sales velocity. For the first six months of the year, total sales were just 10% ahead; in every other year on record, sales have been at least three times unsold stock, usually five to fifteen times. Whichever way you look at these figures, it’s clear that at the moment, effective demand is weak. That’s not a market in which developers will be keen to build more.

A further complication is where the unsold stock is. The top five boroughs for unsold stock are Tower Hamlets (556), Wandsworth (455), Westminster (315), Barnet (294) and Hammersmith & Fulham (274). These are not low-value boroughs, to say the least; the issues seem to be that the unsold stock is generally in locations where affordability is most stretched or where the market was most investor-dependent. (It’s notable that starts are clustered in cheaper, outer boroughs – see below – meaning developers are shifting away from more expensive, more flat-orientated Inner London).

New build has become more unaffordable. Part of the issue may be that new build prices have, despite the build-up of new build stock, risen faster than in the second-hand market. According to the Land Registry, new build pricing in London is now 7.8% higher than three years ago, compared to 0.3% for the market as a whole. Even over the past year, new build prices have risen by 3.4%, compared to 0.7% more generally. (This figure is based on a dwindling sample of new build sales, so it may be less robust, but it is worth noting that this trend is backed up by the Nationwide index at the national level, where new builds have increased in price by 6.2% over the past three years, compared to 0.9% in the wider market.) This reflects developers attempting to recoup the much higher costs – potentially lossmaking – that have been produced by the very different construction and debt conditions of the past few years. But it also means that sales fall and unsold stock builds up, as we are seeing.

End of Help to Buy. Help to Buy, the government’s equity loan scheme for new build sales, was not as important in London as elsewhere, but nevertheless, an estimated 27% of private housing completions over the scheme’s lifespan in London involved it. (This compares with a third in, for example, the South East). The end of the scheme for units completing by mid-year 2023 clearly impacted new build sales, which in that year were 35% below 2022 levels, and have not recovered since.

Build-to-Rent. According to Molior, there were just 37 build-to-rent starts in the first six months of the year, compared to 2,626 in 2024 and a 10-year average of 5,600. Build-to-rent faces similar problems in costs and viability to ‘for sale’ development, but it is complicated by the funding/investment side. Put simply, although residential remains a priority sector for many funds, which see the long-term issues around a growing population and a structural lack of supply, other asset classes, such as government bonds, currently look more compelling. So, the flow of capital has generally slowed. More specifically, yields for build-to-rent in London, at 4-4.5%, are lower than for any other sector, which, at a time of higher risk-free rates, is problematic. This also explains why build-to-rent development in the main regional cities (yields 50bps higher) has continued, albeit at a slower rate.

3) Regulatory Burdens increased while the market thrived, but have not yet been reduced despite weaker activity

Affordable Housing requirements have become too high and inflexible, given current market conditions. London has historically set relatively high affordable housing requirements (35%, compared to a minimum NPPF expectation of 10%). The package announced by the government, in combination with CIL reliefs and higher grant levels (see below), will boost viability, but a more flexible approach needs to be taken in the longer term.

CIL contributions represent a further burden. The Mayoral Community Infrastructure Levy (MCIL), which back-funds the Elizabeth Line, can be a prohibitively high amount in the current market, particularly when combined with local CIL levels.

Lack of capacity from Registered Providers (RPs). A further complication is the difficulty in finding an RP to take on any affordable homes, as most housing associations have financing issues themselves and are focused, in any case, on the issues around their legacy stock. The Home Builders Federation (HBF) reported in October 2025 that there were 17,432 Section 106 affordable units that remain unallocated. It is unclear how many of these are in London, but it is likely to be a high number.

The Building Safety Levy will be introduced next year. In addition to the above measures – which are already in force -there is another important factor coming into play next year. As of October 1, 2026, developers of residential properties of more than 10 dwellings (excluding affordable housing) will be liable for this charge at the building control stage. It will be calculated based on the size of the development, but there will be different rates for each local authority level. It seems likely that they will be higher on average in London.

The Residential Developer Tax. In addition to all the above, developers of residential property are liable for a 4% additional levy on their profits. While this does not impact the viability of particular schemes, it makes developers more risk-averse and conservative. It also deters new entrants, reducing competition.

4) The supply of land is falling as a result, and developers are becoming more risk averse

Landowners are not willing to drop their prices. Many owners of land are not in a rush to sell and are happy to sit out what they see as market cycles. In most cases, they will have a minimum price in mind, set by earlier market conditions or by the value of their asset in its existing guise, say a supermarket. At the moment, these are radically lower than a few years ago, which incentivises many to ‘sit tight’. Even if these conditions persist, it takes some time for their expectations to adjust. In the meantime, developers cannot feasibly meet the prices being demanded; if they do, they risk pricing themselves out of the sales market, as may already be happening.

The problem is compounded by affordable housing requirements, which are based on market conditions that no longer exist. This has forced land prices even lower – in some cases, below zero. Together, this means that the pipeline of land for development will be constrained.

Planning Delays and Costs. The UK’s already infamously complex, slow and costly planning process has become even more so over the past few years. This is a further drain on viability, but it also slows down the supply of consented land into the system. This is a result of the introduction of additional requirements (such as biodiversity net gain, which often has higher costs on long-term derelict sites), but also because councils have lost a lot of planning staff through budget cuts. Other services have been more protected. Even though funding has improved over recent years compared to the nadir of 2018/19, it remains 25% below the 2010 level.

Increasing risk aversion. Growing regulatory burdens, volatile construction costs, and an uncertain economic outlook are leading developers to focus on a smaller number of ‘easier’ schemes – largely housing-oriented sites away from London.

The Big One: The Building Safety Act and the Gateway Processes. The Building Safety Act introduced new requirements for residential buildings over 18 metres or six storeys. These include, for example, a second staircase to aid evacuation, which adds a not insignificant amount to build costs, especially in mid-rise schemes.

But more importantly, plans for such developments also need to be submitted to the Building Safety Regulator (BSR) for approval. This consists of Three Gateways. Gateway 1 relates to pre-planning guidance. The key issue is at Gateway 2, which is a ‘hold point’ where “construction cannot begin until the Regulator is satisfied that the design meets the functional requirements of the building regulation”. Plans need to outline exactly how compliance will be met.

Figures published in July 2025 showed that of the 193 applications received since the BSR was set up in 2023, only 64 had been determined by March 2025. Of these, only 15 had been approved, with 17 rejected, 12 withdrawn, and 20 viewed as invalid. This means that only 9% of proposed tall buildings hoping to start construction between Autumn 2023 and Spring 2025 have been permitted, in theory, to start.

A Freedom of Information (FoI) request submitted by the Architects’ Journal showed that, as of August 2025, there were still some 72 Gateway 2 applications which had been outstanding for more than 12 weeks – the target timescale for decisions – covering 18,436 homes. In scheme terms, more than half of them (37) were in London. Building magazine is reporting that the average sign-off time is nine months.

Gateway 3 occurs at completion as part of the building control process. The numbers reaching this stage are far lower – presumably because so many have failed to get past Gateway 2. Figures here are harder to get hold of, but in February, figures emerging showed that only 1 in 4 projects reaching this stage had been approved. One completed 487-home development in Ealing sat empty for months, gaining approval in late September this year. There is a danger that even if Gateway 2 accelerates, blocks of flats could be completed and standing empty long term if this third check proves to be equally delay-producing. This risk will clearly reduce the appetite for development.

The government has vowed to speed up the process, but it is unclear how and when this will be done. The process is understandable given the Grenfell tragedy that led to the original act, but it is having a distorting effect on the market. In particular, developers are avoiding schemes over six storeys, meaning:

- London is disproportionately affected, as delivery in the capital is skewed towards higher-rise buildings

- Inner London is particularly impacted, as delivery is even more skewed here

- This is further pushing developers towards more low-rise and suburban schemes outside London

THE END OF MODEL?

All these factors (and particularly the Gateway 2 delays and costs) are responsible for the delays. But perhaps the problem is deeper: the model that has underpinned London development for the past two decades is increasingly under duress. A reconsideration may be well overdue.

This ‘model’ is based on a set of assumptions: that land values would always increase in the medium term, that they could be tapped in some way to provide very high levels of affordable housing and other social goods, and that the expensive private homes driving the whole process would sell – with the early stages sold to off plan to (largely overseas) investors. This latter stage would ‘unlock’ the scheme, enabling debt at viable levels.

This does not mean that this model will never be viable again. But it would be misguided to think that it can return in the near future to such an extent that London can deliver more homes, let alone reach the government’s target. A new approach will be needed if London can deliver in the medium term.

London’s Homebuilding Crisis: Policy Challenges, Market Pressures and Solutions

1) Introduction

London is facing a housing construction crisis. In the first nine months of 2025, just 3,248 homes (source: Molior) began construction – barely 11% of the recent average and under 5% of the government’s annual target. Affordable housing delivery has fallen even more sharply. This collapse is not just a statistical anomaly; it signals a systemic failure with far-reaching consequences for Londoners’ living standards, the capital’s economy, and the resilience of its construction sector.

This research is intended for policymakers, developers, investors, and housing professionals seeking to understand and address the structural challenges facing London’s residential market. It investigates the root causes of the slowdown, from regulatory gridlock and deteriorating development viability to weakening demand and a broken affordable housing model. It argues that London’s current residential development framework, built on assumptions of ever-rising land values, investor-led demand, and rigid planning obligations, is no longer fit for purpose. In response, it sets out a series of urgent policy recommendations and proposes a new, more flexible and responsive housing model.

The crisis also reveals a deeper structural issue: the disconnect between planning policy, market realities, and actual outcomes. This paper highlights emerging ideas that seek to bridge these gaps. Our concept of a more connected model of residential development, and our conviction, Residential: Connected, can support many of these ideas. This model seeks to align public and private sector efforts, link viability with long-term value, and place people and place-making at the centre of delivery. These principles underpin a more integrated, outcome-focused approach that can help unlock stalled sites and rebuild confidence in the system.

How to Navigate This Research

This report is structured to help readers understand both the immediate causes of the slowdown and the deeper structural issues at play. It begins by diagnosing the crisis, then explores the failure of London’s current development model from the current perspective, and finally sets out actionable recommendations for policymakers, developers, investors, and housing professionals.

You can explore each section using the chapter linked via the navigation panel on the right, or you can view the research in PDF format by clicking on the button below. The next chapter provides an overview of the research and our conclusions.

For more information, please contact our Head of Research & Insight, Jon Neale or our Head of Residential, Adrian Owen.

A Package of Support for Housebuilding in the Capital – Unlocking Sites, Restoring Confidence?

The announcement on 23rd October 2025 by the Housing Secretary and Mayor of London represents a decisive intervention to kickstart the capital’s flagging housing delivery.

At the heart of the proposed package of support for housebuilding in London is a recognition that the current system has become unviable for many developers. Construction costs, financing pressures and Gateway approval timescales have left hundreds of consented sites on hold and deter landowners and developers from bringing new schemes forward.

This package of new measures is welcomed, but in isolation will not solve the structural economic issues impacting the housing market. Nevertheless, we believe these changes will bring more confidence to the sector and will unlock some stalled development sites and hopefully pave the way for future growth.

There has been some negative press suggesting these changes don’t go far enough. But as matters within the control of planning guidance, they feel fair and proportional, and critically allow enough time to translate to meaningful action. However, the details to be set out at the consultation stage will be critical to the success of these interventions.

Such questions could include:

- What form will the gain-share review take without the presence of viability testing?

- How do these measures interact with the standard 35% Fastrack for CIL relief and grant?

- Can you apply equivalency under the new route?

Our summary of the announcement’s core components can be found below, including additional analysis by our sector specialists.

Central London Planning Policy Update Q3 2025

This briefing paper provides an overview of recent planning policy news and recent / emerging consultations or changes within the Central London boroughs, as well as updates from the Mayor of London and the Government in relation to the capital.

Q3 Planning Policy Headlines

- The GLA has reopened a further period of consultation on Towards a New London Plan, covering policies on housing, employment, transport, and open space, open until 2 November 2025.

- The Draft Camden Local Plan was submitted to the Planning Inspector on 3 October 2025 for examination, which is likely to be ongoing over the coming months, with adoption expected for Winter 2026.

- Westminster City Council have published all representations regarding the proposed Main Modifications to the City Plan Partial Review, with adoption expected later this year. Further Retrofit guidance has been published for consultation to support the new policy.

- Westminster City Council has opened a ‘Call for Sites’ (open until 20 November 2025) for locations that can deliver 50+ homes, 2,500 sqm of commercial floorspace, qualifying mixed-use schemes, or infrastructure identified in its Infrastructure Delivery Plan, to help them produce the new City Plan.

- LB Wandsworth have completed Regulation 19 consultation and independent examination for the Local Plan Partial Review, which will be subject to public hearings in November 2025.

Click below to read the update in full.

Our Methodology

DOWNLOAD THE 2026 HANDBOOK

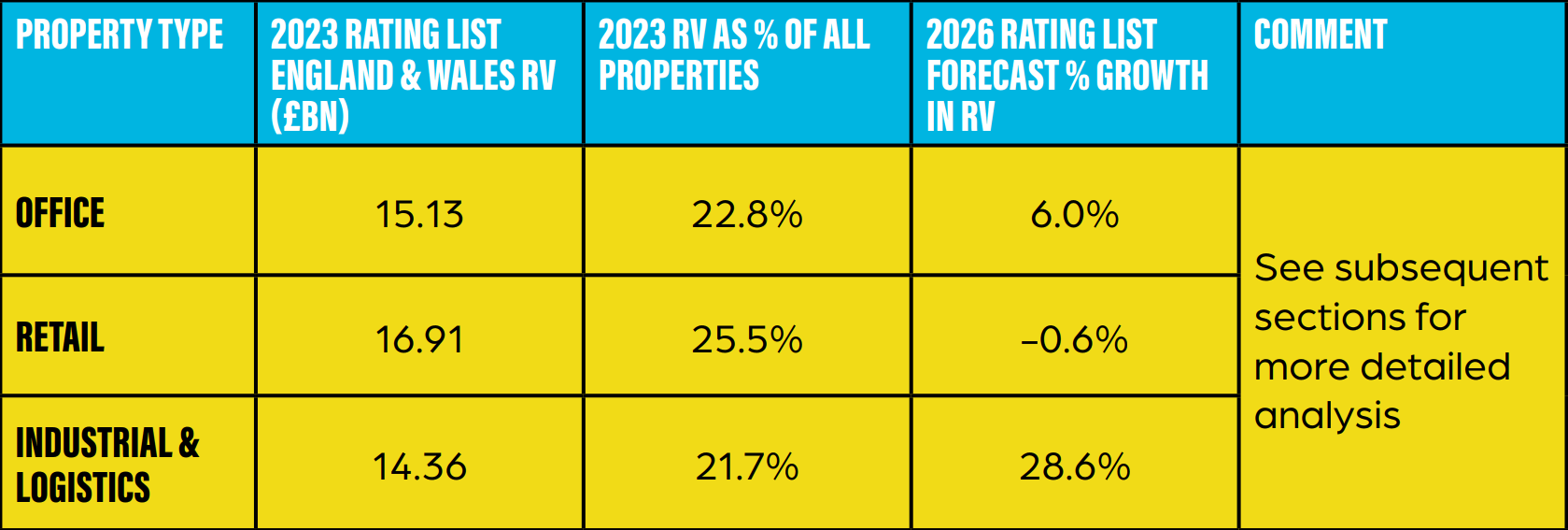

The research uses the established benchmark of the Quarterly MSCI UK Property Index, which contains £24.8bn of retail properties, £26.8bn of offices and £40.7bn of industrial & logistics. This provides valuation-based estimates of market rental growth, broken down by segment and location, over the three years to 1 April 2024 by sector.

The segments show very divergent patterns, a result of the impact of various broader movements on the differing property markets and geographies. In broad terms, logistics, driven by the growth of online retail and the move to greater inventories, has seen very strong rental growth; offices has seen positive, but very modest growth (behind inflation); and retail is still falling, albeit modestly and with a divergence between a relatively robust out-of-town and a more troubled in-town segment.

Within the following pages, we do not address likely value movement for properties valued with reference to build cost or profit (and this range of properties is extensive) however, we do anticipate:

Properties valued with reference to their land and build costs – likely to see above-inflationary increases reflecting a number of factors, primarily:

- Build costs, which according to BCIS have risen by approximately 19% over the three-year period since the last Revaluation

- Labour costs, where the Office for National Statistics points to a growth of 15-20% across the period

Properties valued with reference to their profitability – often linked to properties with a high degree of public interaction, 2021 values frequently reflected Covid restrictions and consequential trading impact. April 2024 values will reflect the post-Covid bounce back, which is likely to mean significant increases for many.

Forecasting liability

Understanding rateable value and multiplier movement is critical in forecasting likely movement in liability at individual property and portfolio levels.

The VOA will publish the Draft Rating List in late 2025, which will be the first time it publicly reveals its views on value levels at a local, regional and national level.

Until this stage, it is not possible to predict individual property values accurately. Instead, the following pages provide greater clarity in respect of likely trends in regional and national value movement and consequential rate multipliers using averages across a broad range of properties.

In summary, we forecast an overall weighted increase in value of 9.1% across the prime property classes: office, retail and industrial & logistics.

Notwithstanding the above, we anticipate that the overall % growth in the aggregate rateable value included in the Rating List to be greater than this, reflecting additional sectors not listed above and specifically those valued with reference to their build cost or profitability. As a result, we estimate that the overall increase will be in the range of 12.5%-15%.

The conclusions of our research are explored in more detail on the following pages.

Rate Multiplier

The current standard multiplier is 55.5p/£ (49.9p/£ where the RV is less than £51,000).

The Revaluation will rebase the multiplier to reflect national movement in rateable values.

The general principle in resetting the multiplier is that other than to reflect inflation, the process should be revenue neutral, ie Treasury collecting the same amount in real terms in 2026/7 as they had in 2025/6 (the last year of the 2023 Rating List).

Assuming an overall increase in Rateable Value of say 15% and reflecting current CPI inflationary levels we are predicting a standard rate multiplier of approximately 50p.

It is important to note that lower multipliers currently exist for properties with RVs below £51,000 and individual property liabilities will be impacted by reliefs and supplements; for 2026 there will be the added complication of differential multipliers.

What should businesses do now?

DOWNLOAD THE 2026 HANDBOOK

First, understand where your assessment might move to. Although draft values will not be made public until autumn, a preliminary review before then can highlight areas of likely concern.

Second, explore early opportunities to mitigate. Ideally, the system should not be complicated by reliefs and differential multipliers, but in reality, ratepayers should make sure they make the best use of them to their own advantage.

Finally, it is more important than ever to ensure the facts upon which the Valuation Officer has based their assessment remain correct. Until such time as the planned ‘Duty to Notify’ of physical changes to the property or its tenure is widely introduced from April 2029, the potential remains for rateable value to be based on historic, incorrect data. Ratepayers would be well placed to review their current valuations and ensure the best starting point for future reviews

The system will continue to change. With further statutory reforms and duties planned, this pace is only set to increase. Challenging as it is, the more that businesses do now to get ahead, the more manageable the impact of these 2026 changes will be, both in terms of the accuracy of bills and the time to forecast, prepare and mitigate for their impact.