The structural drivers that will see the industrial & logistics market through uncertain times

read in PDF format

This paper explores the tension in UK industrial & logistics real estate between short-term capital market disruption and strengthening long-term fundamentals. The Iran War and the closure of the Strait of Hormuz have intensified trends on both sides of this equation, adding to short-term uncertainties while strengthening some of the structural drivers behind the sector.

Short-term disruption, not demand collapse:

The Iran energy shock has reset expectations for yield compression. This will stall transactions through a reset of price discovery, rather than a deterioration in occupier fundamentals.

Demand drivers are long-term, structural and have been intensified by the war:

- Larger inventories: Supply chain vulnerabilities have been brought into even greater focus by ‘choke points’ such as Hormuz. This is likely to reinforce the shift to larger inventories (‘just in case’) and commensurate demand for industrial space.

- Defence Spending: The Iran and Ukraine wars have highlighted both increasing global instability and the weakness of some aspects of UK defence. The UK’s Defence Investment Plan, published at the end of June, lays out £298bn of spending over the next four years, with the aim of it reaching 2.7% of GDP by 2030. With the emphasis on new autonomous and drone technologies, as well as new air defence systems, “this will generate additional demand for industrial & logistics space, with second-order effects on the wider supply chain.

- Energy Security: The demand for battery storage – which is becoming cheaper and increasingly practical at scale – will increase demand for industrial sites and crowd out traditional uses.

- Tech Spending and Hyperscaling: The investment by major tech players in data centres looks set to continue, despite concerns over sustainability – providing a further source of demand and competition for B2/B8 uses

But supply will be cyclically constrained for the foreseeable future: Rents remain robust, reflecting a shortage of modern, fit for purpose space despite elevated headline vacancy, as much of this empty stock is functionally obsolete. These shortages will intensify over the next 2-3 years as development has slowed sharply due to elevated cost and uncertainty and there is little sign of it picking up in the near term. This will favour developers and investors able to deliver into this market.

Strong relative positioning in a higher-rate world: Even if higher rates persist as a “new normal,” industrial & logistics is the best placed broad commercial property sector to weather it, given the combination of constrained supply and structurally driven demand.

11 Key Takeaways from UKREiiF 2026

At this year’s UKREiiF, one theme came through louder than any other: the industry knows what needs to be done, now it needs to deliver.

Our team has distilled the key discussions, debates and insights into a focused set of takeaways that we believe every property professional should have on their radar right now.

From reframing housing as a critical economic engine, to recognising that viability is as much a communication challenge as it is a technical one, the conversations this year pointed to something bigger.

The sector is shifting from ambition and intent towards action and execution. There is a growing recognition that unlocking delivery will require more than policy changes or capital alone. It will depend on stronger partnerships, clearer messaging, and a more joined-up approach across the industry.

Click below to download the full report to explore all 11 takeaways.

Geopolitical Shocks Delay Recovery but There Are Pockets of Resilience

SUMMARY

- The property market entered 2026 with momentum building, but the Iran conflict has pushed up energy prices, inflation expectations and bond yields, disrupting the recovery. This will be intensified by a potential Labour leadership contest.

- These factors are likely to weigh on pricing, investment activity and residential development over the next two quarters.

- Even so, the downturn is not uniform: leasing markets are likely to remain relatively robust, particularly London offices, and the residential rental market may strengthen as supply becomes scarcer.

- Much depends on the length of the Strait closure and the struggles within the Labour Party, as well as the impacts on the real economy; with GDP growth coming in at 0.6% in Q1, and some other indicators remaining strong, they could be slightly more limited than feared.

EARLY MOMENTUM

Back in early February, it seemed as if things might finally be looking up for the property market.

Firstly, inflation was clearly on the way down. That meant the Bank of England would be able to cut rates by 50bps or even 75bps over 2026, and gilt and swap rates would fall (albeit not at the same pace).

Lower risk-free rates would make existing property pricing look more attractive to buyers, while debt was set to become accretive again as costs fell.

Secondly, the economy – while hardly looking like it was entering boom territory – appeared to be on the verge of a fragile and gradual recovery, driven by lower inflation and falling energy costs.

Finally, many occupier markets were seeing some reversal in fortunes. Industrial leasing appeared to have bottomed out and was increasing; regional offices were showing some signs of life; and residential development starts were trending upwards, albeit from an unprecedentedly low base.

In turn, investors were responding. Total volumes in Q4 reached £20.4bn, the highest total for almost three years. All segments were seeing an upward tick in activity, but it was most notable for the residential market. Build-to-rent investors appeared to have returned, while confidence was building in offices, in Central London in particular.

eNERGY sHOCKS

And then, on February 28th, the United States began “Operation Epic Fury” with a string of missile strikes on Iran and the assassination of the regime’s Supreme Leader. In response, Iran attacked the US’s Gulf allies and effectively closed the Strait of Hormuz.

The Strait is one of the world’s most important shipping lanes. It carries about 20-25% of the world’s oil exports and about 20% of its LNG exports. While the UK and Europe are less dependent on Strait-carried oil than Asia – although they are affected too through global pricing and shortages of some refined products – the gas element is potentially more important, especially for the UK.

Brent Crude prices rose from around $60 to over $100 and have remained volatile given the level of uncertainty over the future of the conflict. Meanwhile, European gas prices jumped by around 70% in the days after the war and have since fallen back to around 50% above pre-conflict levels.

While these are huge jumps, it is important to emphasise that it is much more modest than the shock that occurred after Russia’s invasion of Ukraine in 2022.

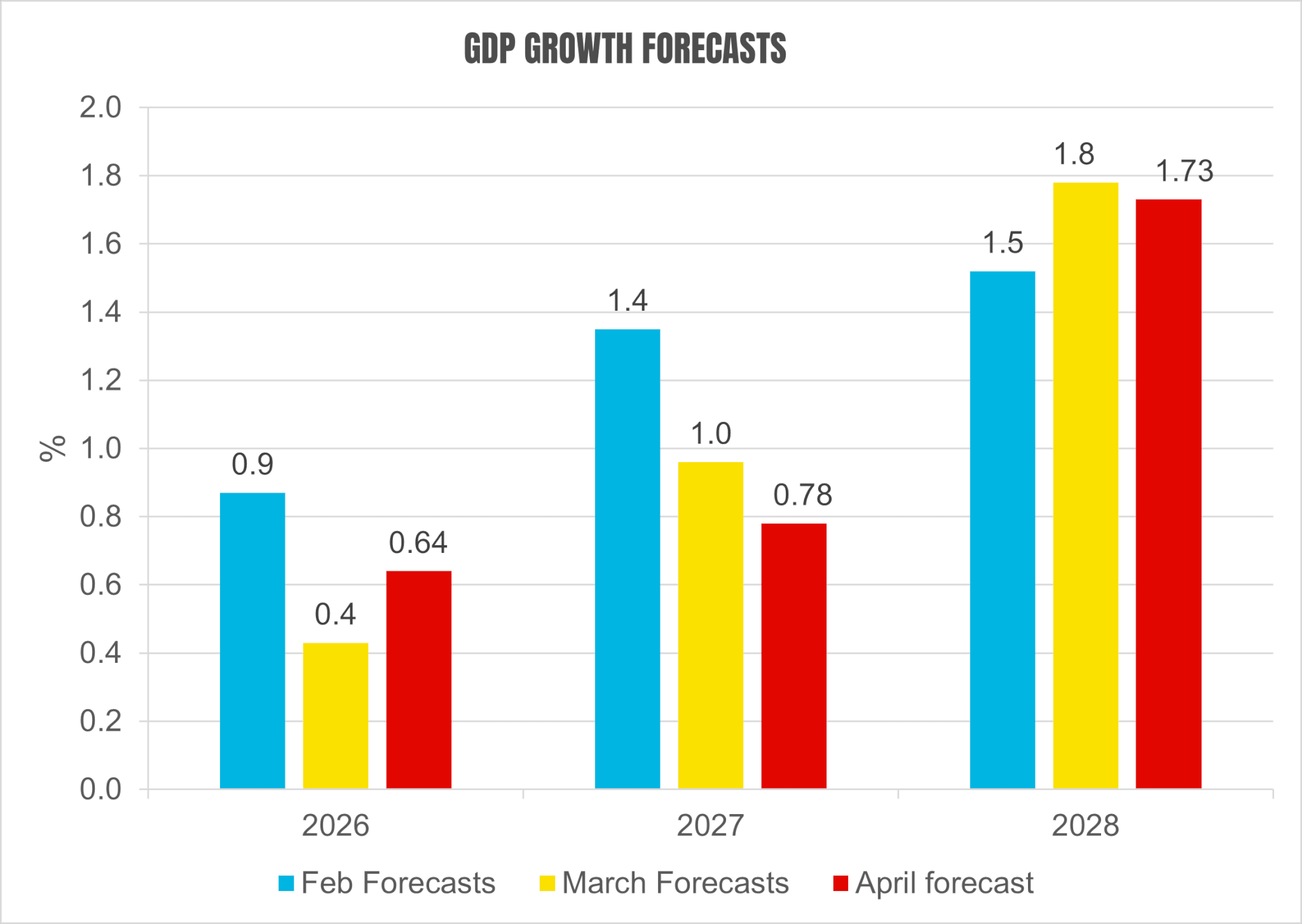

This will all weigh on the economy, as it will increase costs for both business and households and reduce investment and consumption compared to expectations. Oxford Economics has cut its forecasts for 2026 from 0.9% in January to 0.6% in April.

Source: Oxford Economics

The April forecast for 2026 has been tweaked upwards slightly as a result of strong outturns in the year so far. However, the 2027 forecast was reduced from 1.4% in February to 1.0% in March, and then taken down another 20bps to 0.8% in April.

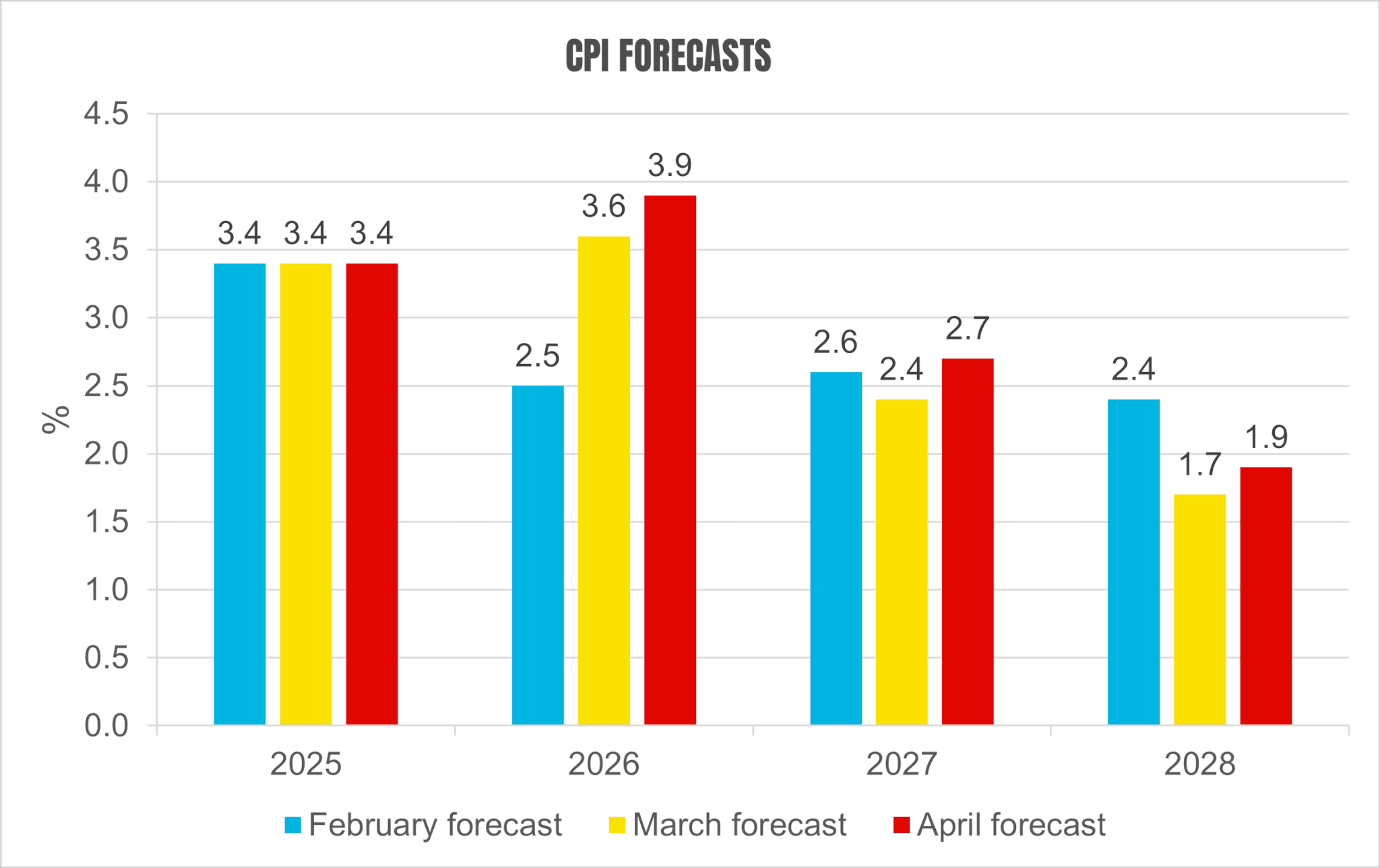

This is obviously serious, but the more dramatic impacts have been on inflation expectations. Annual change in CPI was trending downwards in the second half of last year, with forecasts pointing towards 2.5% by the end of 2026.

This would give the Bank of England room to cut base rates, with two or even three 25bps slated at that point for the year ahead.

But Oxford’s forecasts for CPI in March, in the wake of Iran, saw that rise to 3.6% – a figure that was subsequently adjusted upwards to 3.9%. This is partly a result of the direct impact of higher energy costs, but also the indirect effects on goods through increased transport and materials costs (oil and gas are important feedstocks for some manufactured goods).

Source: Oxford Economics

The Monetary Policy Committee (MPC) will be very aware of these potential “second-order” costs, particularly if they shift consumers’ price expectations. This would lead to demands for higher wages and a potential wage-price spiral. The MPC has been criticised for failing to act quickly enough after the energy shock caused by the Ukraine war, so it will be keen not to make the same mistake again.

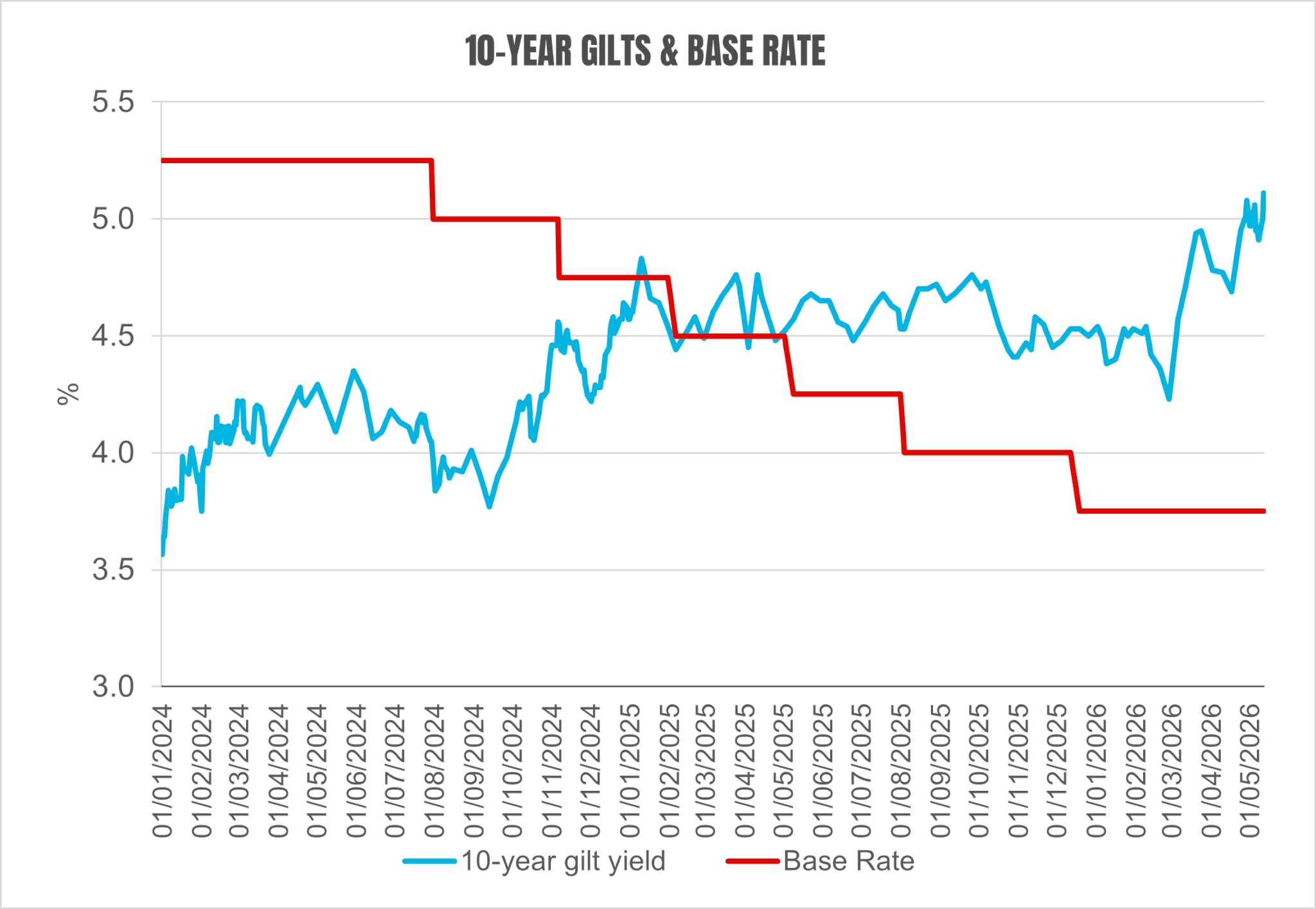

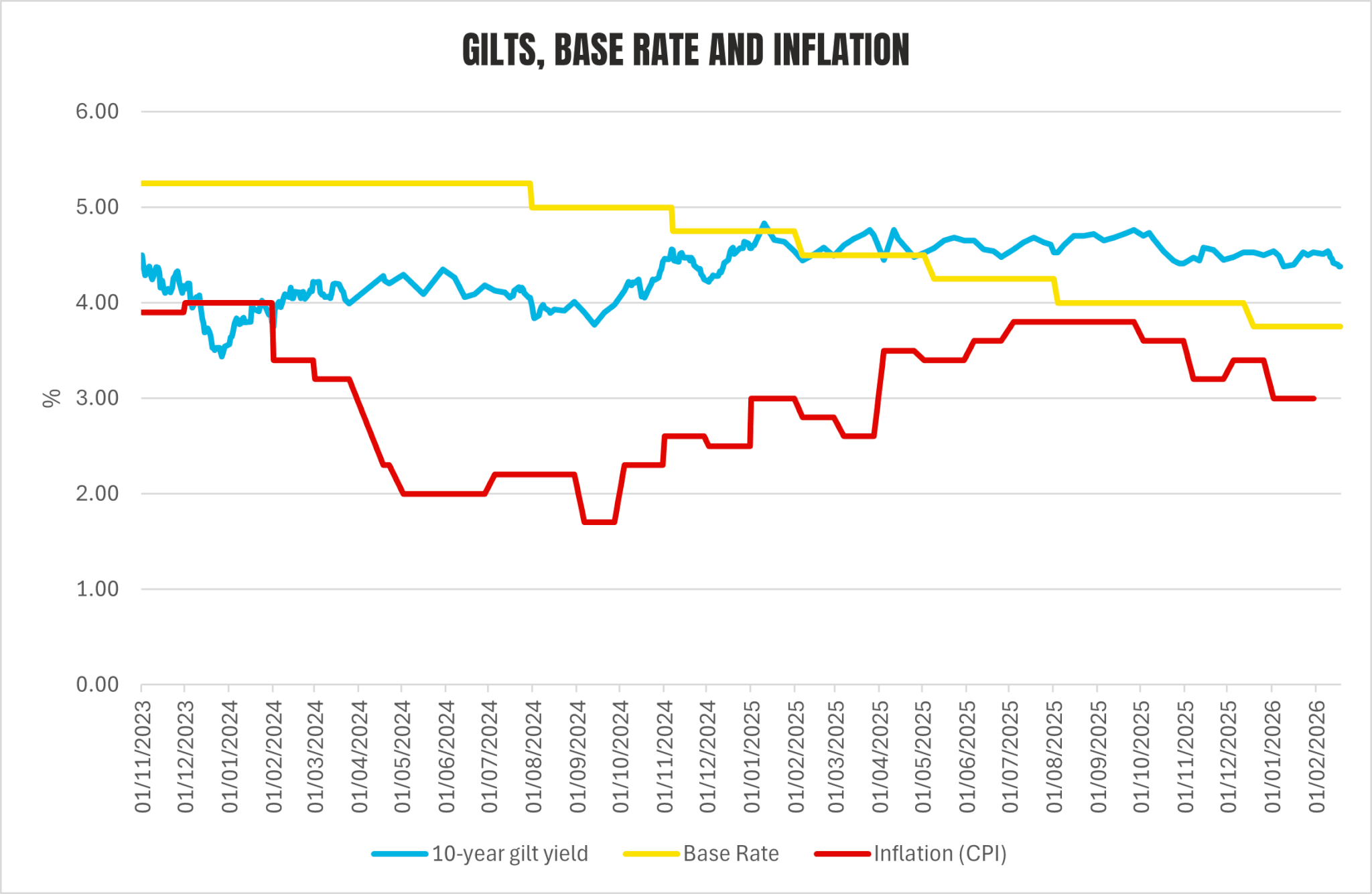

Higher inflation means that bond investors will demand more in interest to compensate for that erosion in value. But there’s more: slower economic growth points to lower tax revenue, which further casts doubt on the UK government’s fiscal sustainability – an issue which was already of concern to bondholders.

The resulting “sell-off” of this government debt led to an increase in supply and a reduction in demand – meaning a fall in price, or a rise in yields as they move in opposite directions.

The local elections have added further uncertainty to this picture. A Labour leadership contest is looking increasingly likely, and bond investors will be concerned that Keir Starmer will be replaced by a leader with a higher-borrowing, higher-spending instincts. This has added another risk premium to gilts.

Source: Bank of England / MarketWatch

Market Impacts

The problem for property is that 10-year gilts often represent the “risk-free rate” against which fair value is calculated. The greater confidence in the market at the beginning of the year was due to the anticipation that yields would start moving downwards. Not only would that make it easier for buyers to meet vendor expectations around pricing, but it would also give them the confidence that their property would be worth more in the years ahead.

That expectation has been, to put it bluntly, shattered, at least in the short to medium term. The hike in bond yields suggests that property yields will, at best, stay where they are – at least in aggregate (some sectors are more insulated than others, see below).

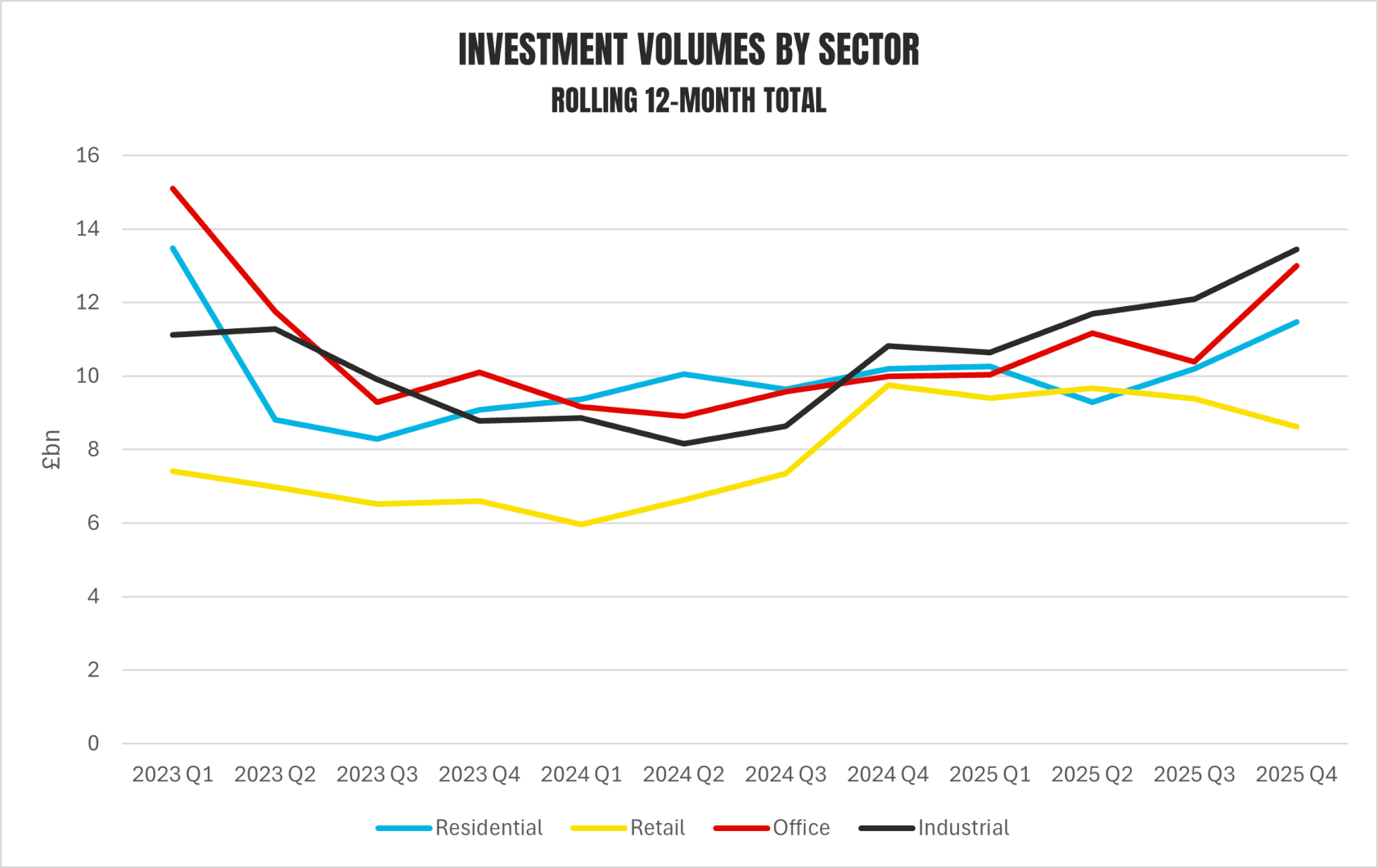

This suggests that the increase in transaction volumes seen at the end of last year will not be sustained. And indeed, volumes in Q1 2026 came in at £9.0bn, the lowest total since Q3 2023. All sectors were hit, except residential, which continued the strong activity it saw in Q4.

To be fair, it is unclear whether this is a direct result of the Iran war, which after all, broke out at the end of February, but March tends to be the strongest of the three months for deals.

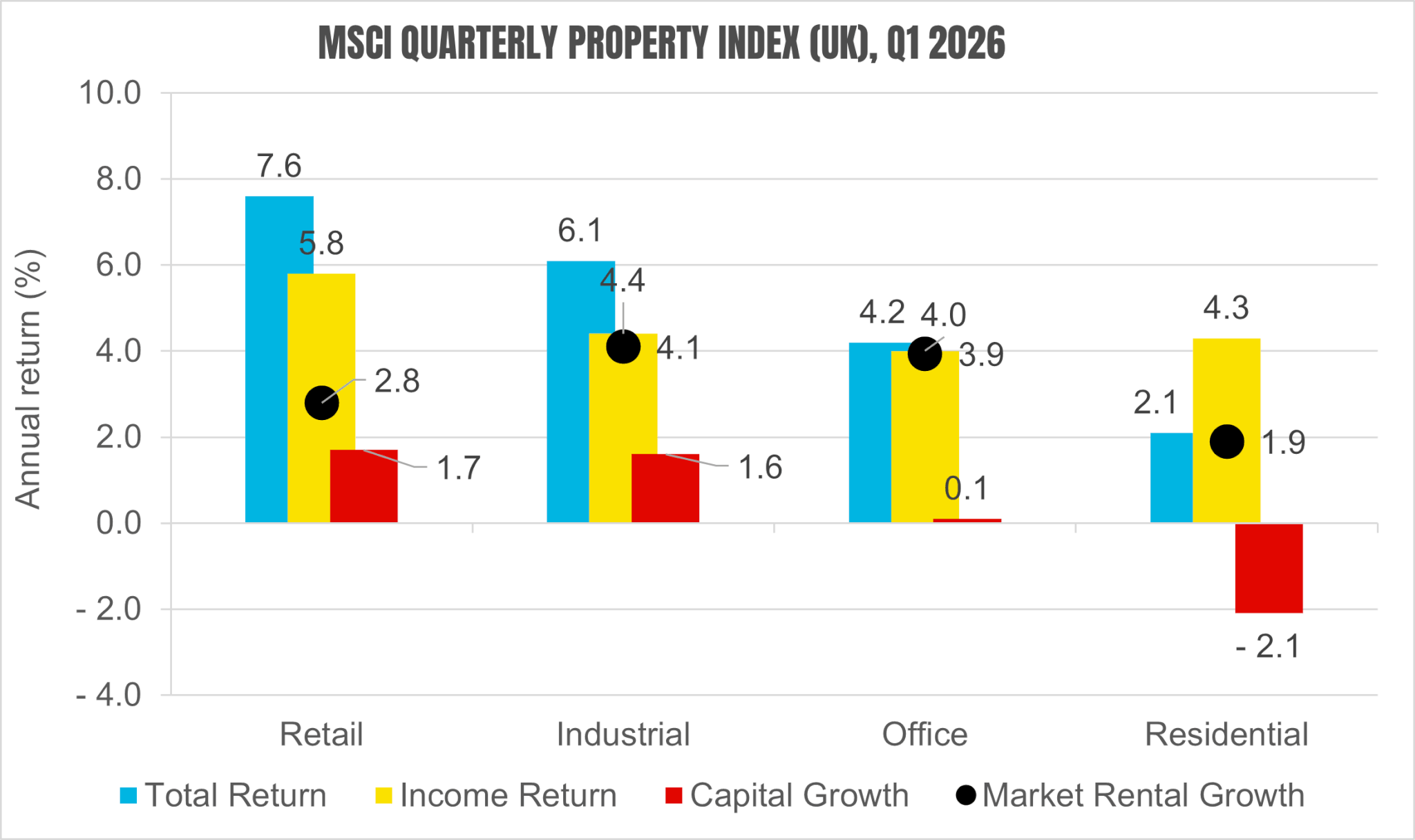

MSCI Total Returns slipped back for retail and industrial, from 8.4% to 7.6% and from 7.2% to 6.1% respectively. This was driven by a sharp fall in capital growth. Residential saw a similar slippage despite the interest, from 3.1% to 2.1%, with negative capital growth intensifying from -1.4% to -2.1%.

Offices, however, moved in the other direction; capital values are now flat year-on-year (compared to -1.4% at Q4), and this has pushed total returns up by 70bps to 4.2%. Yields in some office segments had reached quite high levels and are presumably less affected by the shifts in bond yields, and in some areas, confidence is returning to the market more generally. The fact that the West End is seen as a safe haven for wealth preservation is another factor.

Source: MSCI

Some of this may reflect base effects – there was quite a lot of capital growth back in Q1 2025, but more modest figures for the rest of the year. This historic growth has fallen out of the figures for this quarter, making the shift to weaker growth look more recent than it is. But it is also an indication that the war is beginning to have an impact on pricing and confidence.

The leasing market was more robust. Across both office and industrial markets, leasing remained in line with the long-term average, with vacancy generally now on a falling trend. This should prevent sentiment and rental growth from deteriorating rapidly.

The residential market is likely to be most affected by the war in Iran. Investment will be subject to the same forces as elsewhere in the property market, but it has the additional issue of the mortgage market. Shortly after the war broke out, thousands of mortgage products were removed from the market, and average rates, which had been strongly trending down since the start of 2025, have now risen by 50-100bps depending on length and LTV.

This will clearly impact the demand for property, further reducing developers’ ability to build much-needed homes. Viability for such development will also be impacted by higher debt costs and materials costs (as it will across other sectors). This will not have an equal effect on all development types, as material mixes will differ.

There is a brighter outlook for one part of residential, though. RICS surveys indicate increasing unsold stock among agents and decreasing sales and enquiries, but the rental market is going in the opposite direction. Stock is decreasing and tenant demand is increasing.

This is perhaps unsurprising, as some people who can’t (or won’t) buy at the moment are forced into renting. Meanwhile, there is some evidence that the stock of rental property is reducing as landlords exit the market, as a result of the cumulative effect of legislation, as well as the upcoming Renters’ Rights Act.

Together, this suggests that rents – which have been flat for the past year to 18 months – may begin to rise again. Investors have been attracted to the sector not by the short-term dynamics, which have been difficult given costs and yields, but by the long-term demographic tailwinds, structural shortages and portfolio diversification benefits. Rising rents could ensure that, despite all the issues elsewhere, it remains the target of investor interest.

Industrial – still fashionable globally with investors – and central London, where activity continues apace amid a shortage of new good quality stock, also look resilient.

cONCLUSION

The market is likely to, at best, remain weak over the next quarter or two. The course of the war and the blockades are uncertain– as is the degree to which the economy is impacted. The drama within the Labour Party adds a further negative factor.

The most recent GDP figures, out at the time of writing, show a 0.6% expansion in Q1, with GDP per capita rising by a similar amount. There are suspicions that this is a statistical illusion, but there are some other indications, such as retail sales and the PMIs, that growth is more robust than feared.

It is early days in terms of the impact of the energy shock and any leadership contest, of course, and economic prospects have certainly weakened. But the big unknown is to what extent, and how that impacts the property market.

In conclusion, the recovery has been delayed but not necessarily derailed. Pricing will be under pressure, but the leasing market looks generally robust, particularly in London offices. And while the residential sales market is likely to struggle, the rental side may gradually recover, if only because of a shortage of supply.

If you have any questions about this briefing note or any other aspect of the commercial or residential market, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

Central London Planning Policy Update (Q4 2025 & Q1 2026)

This is an overview of recent planning policy developments and current or emerging consultations across the Central London boroughs. It also includes updates from the Mayor of London and the Government on the capital for Q4 2025 and Q1 2026.

PLANNING POLICY HEADLINES

- MHCLG’s Support for Housebuilding (Package of Support) was announced on 25 March 2026. This was after a period of consultation, including temporary CIL relief for qualifying residential schemes and permanent enhancements to Mayoral planning powers. The latter encompassed the introduction of expanded call-in powers for larger or sensitive developments and the allocation of £324 million to establish a City Hall Developer Investment Fund.

- The GLA adopted the Support for Housebuilding LPG, which introduces a streamlined package of emergency measures to accelerate housing delivery in the capital. These include amendments to cycle parking requirements, updates to housing design guidance, and a new time‑limited planning route to support affordable housing delivery. This will apply until 31 March 2028.

- The Oxford Street Development Corporation will become the local planning authority for the area. This is effective from 1 June 2026 and is subject to the parliamentary process.

- Westminster and Wandsworth adopted partial reviews of their Local Plans in January and March 2026. These cover updates to housing and affordable housing policies, with Westminster introducing its new Retrofit First policy.

- Southwark issued the final draft of the Old Kent Road Area Action Plan (AAP) to the Planning Inspector for Examination in Public in November 2025.

- In November 2025, Westminster, RBKC, and Hammersmith and Fulham were all affected by a cyber‑attack. This resulted in the shutdown of core operational functions across their departments. The planning services of all three authorities were affected, limiting their ability to validate applications, undertake consultations, or issue decisions between November 2025 and February 2026. As of 31 March 2026, all three LPAs are fully operational, but face expected backlogs and delays.

Click the link below to read in full.

The Residential Land Survey (2026)

read in PDF format

London’s residential development market remains severely constrained. Housing starts in 2025 (7,480) are under half the long‑term average and far below London Plan requirements. And while developers have been blaming viability, planning delays and the Building Safety Act, this year’s Montagu Evans London and South East Residential Land Survey shows a decisive shift.

Our survey of 53 developers and investors in London and the South East shows that market demand has now become the primary brake on delivery.

Developers report weak buyer confidence, reduced overseas investment, and affordability pressures. As a result, they’re worried about whether they can sell new homes, not just their ability to build them. This is despite the recent resurgence of institutional capital, which has provided a much-needed lifeline.

Format preferences are also changing. Medium‑rise apartment blocks (up to ~6–8 storeys) are now the clear favourite among developers. This reflects buyer appetite and an attempt to avoid exposure to the safety regulations around high‑rise buildings. Low‑rise family housing has surged in popularity too, even among London specialists. However, land constraints limit its potential within the capital.

The land market is adjusting, with most respondents now seeing slight price declines, indicating a greater pragmatism among landowners. Meanwhile, the MHCLG/GLA emergency measures, aimed at boosting viability and still in draft form at the time, are cautiously welcomed. That said, many think the time limits – now extended – would have prevented them from being effective.

Overall sentiment suggests that the market had started to stabilise before the Iran conflict, with expectations of a gradual recovery. Developers were beginning to look ahead to delivering in supply-constrained markets in 2027 and 2028. However, political unpredictability and the decline of the off‑plan investor market have eroded confidence. Many developers call for renewed demand‑side stimulus (e.g., SDLT holidays or Help to Buy) to help absorb smaller flats.

The survey underlines that London’s housing crisis can no longer be attributed solely to planning, viability, or building safety. Demand‑side weakness, particularly for urban high‑rises, is now an equally important constraint. This will require planning authorities to take account of the market’s pivot towards medium‑rise and family housing.

The findings also strengthen the case for the government’s new towns programme. Many of the sites can deliver the mix of mid‑rise and suburban format favoured by developers and buyers.

Inflation Falls, Investment Rises and Key Sectors Begin to Recover

Note: This briefing was finalised on 23 February, before recent events in Iran and the wider Middle East. Energy prices have spiked, and there are concerns that this could lead to higher inflation, slowing down the speed of future base rate cuts and, in turn, the speed of the gradual recovery outlined below. Much will depend on the length of the conflict and the resulting disruption to oil and gas supplies.

Overview

- The UK economy is showing signs of a gradual improvement. While growth is set to remain modest, inflation is easing, and interest rates are falling. This will provide a more supportive backdrop for markets as 2026 unfolds.

- Property markets – and the sentiment around them – appear to have reached an inflexion point. Investment volumes saw the strongest activity in four years in the fourth quarter, led by offices and industrial. This momentum looks set to be sustained, although it will be a gradual improvement, not a boom.

- Across offices, industrial and residential, low construction and robust demand will push up rents over the year, gradually easing viability challenges – although it will be some time before supply can recover more strongly.

A Gradually Improving Economic Backdrop

The final economic reading of the year, GDP growth in Q4, came in with a lacklustre 0.1%, but over 2025, the UK economy grew by 1.3%. This is clearly not spectacular, but it is not terrible either – which might come as a surprise given the economic doom and gloom in the press. Even GDP per capita rose by 1.0% over the year, up from a big fat zero in 2024.

This kind of story is repeated across lots of datasets in both property markets and the wider economy. Slowly, things are beginning to improve, albeit usually at an unimpressive rate. But the results should be more apparent as 2026 progresses.

Take inflation as measured by CPI. December’s outturn was a little disappointing – 3.4%, up from 3.2% in November and slightly ahead of market expectations. But January saw it fall to 3.0%. Since the Summer peak, the trend has been clearly downwards. This is evident in the labour market, which is becoming looser; redundancies are increasing, vacancies are decreasing, and private sector wage growth is slowing.

The Bank of England had adopted a slow and cautious approach to cuts, with forecasters expecting just another two 25bps cuts over 2026, bringing the base rate to 3.25% by year-end. But it’s entirely possible that if all these measures continue trending downwards, there is another 25bps by year-end.

The slightly better economy is, of course, related to falling inflation and interest rates as well as the surprising fact that business investment has been running at historic highs since the pandemic (presumably related to technology). Oxford Economics is forecasting a slightly gloomier GDP growth of just 0.9% in 2026, but this may well be overshot if the wider context continues improving.

10-year gilts, the ‘risk-free rate’ against which property returns are compared, are a slightly different story. The bond market is not only reacting somewhat slower to changes – reflecting the scale of government borrowing both domestically and internationally – it is more volatile. This reflects the UK’s fragility, not just its own poor finances but also the vulnerable position of Kier Starmer and Rachel Reeves. Their replacement with a less fiscally conservative pairing is clearly a risk. At the time of writing, there are also rumours – indications, even – of further ‘events’ in the Middle East, which would also upset the wider picture.

Source: Bank of England + National Statistics + Market Watch

Assuming that none of this derails things too much, then bond yields should follow their choppy path downwards, with the result that property yields gradually become more appealing. Indeed, there is some evidence that the combination of solid if uninspiring growth, reducing rates and strengthening fundamentals in some markets has already been enough to get the market moving again.

Market Conditions Reaching an Inflexion Point

The final quarter of the year saw £17.1bn transacted, the highest total for almost four years. As can be seen below, every sector except retail is now seeing a steady upward trend. The standout was undoubtedly offices, which, with £6bn changing hands, saw the highest total since 2021. This was driven by some large-scale deals in London, with some major international institutions (Hines, Royal London) re-entering the fray.

Source: MSCI

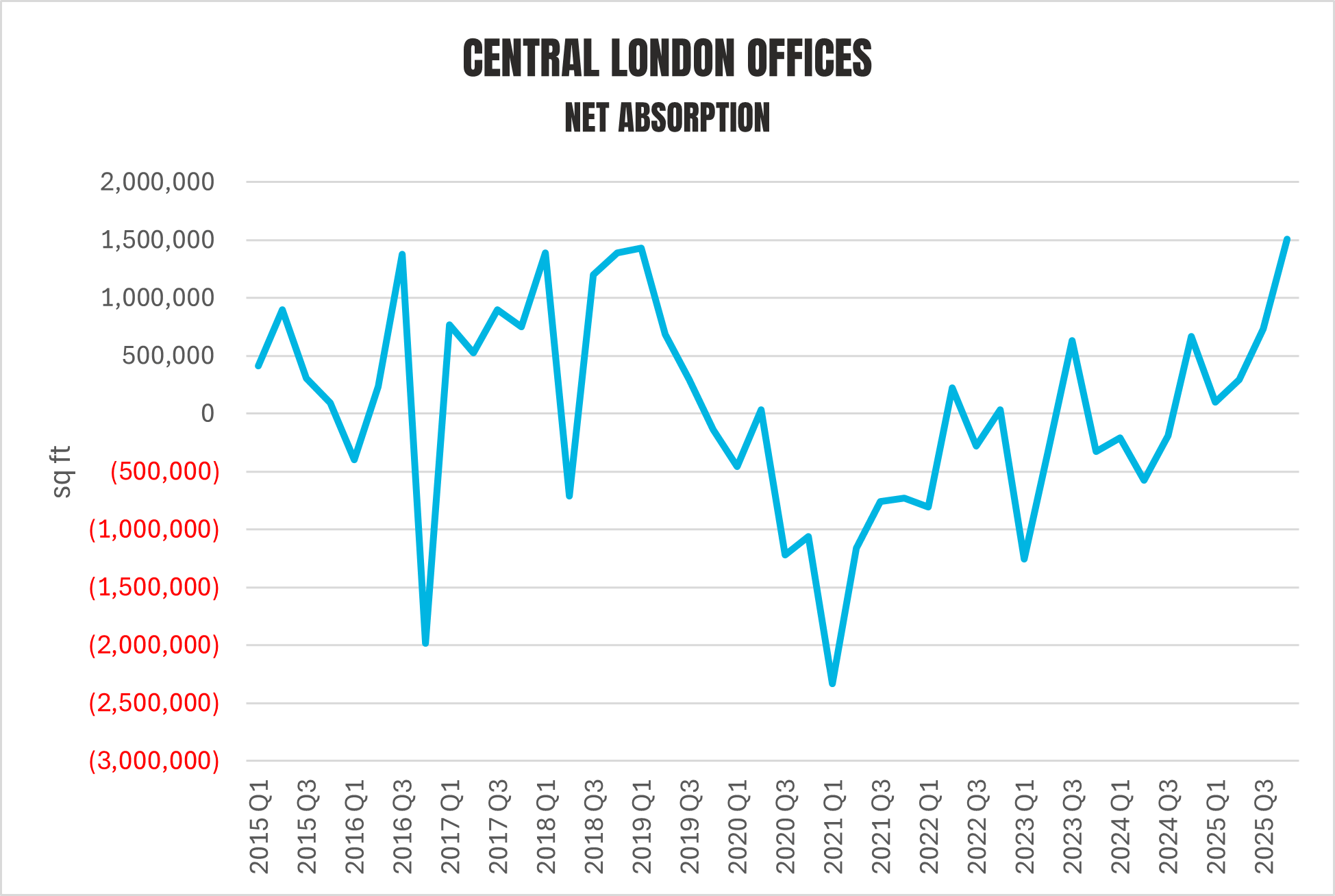

The strong fundamentals in London’s office market have been apparent for a while. Rental growth has been strong, with prime city rents now at circa £100psf, compared to say £75psf three years ago. High vacancy rates obscure the shortage of new, high-quality offices that occupiers increasingly crave. Prelets have increased as businesses have looked to the pipeline, rather than the increasingly obsolescent-looking existing stock.

Net absorption in the Central London market was at its highest on record, even though leasing fell back, suggesting that companies are simply becoming less minded to leave space given constrained availability. Meanwhile, space under construction and construction starts are lower than they were a year ago. But most importantly, investor sentiment has turned, and even if you are sceptical about the arguments around polarisation, the herding effect alone should see both values and volumes rise over 2026.

Source: CoStar

The situation is, if anything, even more stark in the major cities outside London. There have been practically zero starts in every ‘big six’ city except one, and vanishingly small amounts under construction. Manchester stands out as the exception, with 400,000 sq ft started over the past twelve months. It is true that this city had the highest take-up over 2025, but it is not so far ahead of the pack to justify such an incongruity. I do wonder if some of the recent hype over its economy is skewing investment. Now that’s not to say it is doing well – it very clearly is, as any time spent in the city will confirm – but there are some questions over whether the very high figures for productivity growth (see here) are accurate.

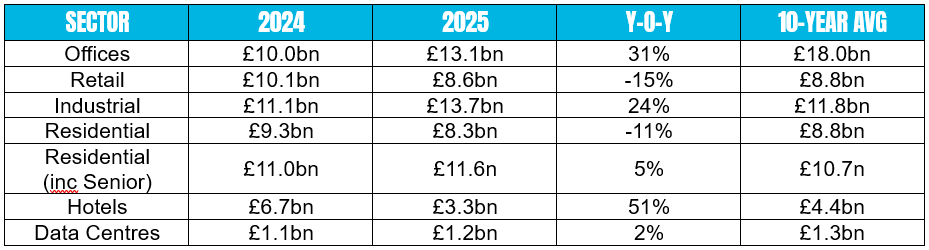

Diverging Sector Performance

Industrial, on the other hand, is still seeing very strong investment, albeit not the great jump upwards seen by offices. The total for 2025, at £11.1bn, was the highest of any sector (just), and represented a 24% increase on 2024. I’ve had mild concerns about industrial for a while; leasing has been muted for two years or so, while vacancy has been rising, and rental growth has slowed considerably.

But over the last few months, a corner has been turned. The pattern is similar to the London office market – falling vacancy and increasing net absorption amid lower leasing activity. This implies that companies are simply not moving because there is insufficient new, good-quality space. (The main difference, though, is that the standout region now is the North-West).

Source: MSCI

So, in offices, residential and industrial, in some locations at least, the market is effectively screaming ‘build’. But that is more easily said than done. Construction costs and development debt costs remain high. Moreover, yields have not yet really budged downwards, partly a result of what’s happening in the gilt market.

The increase in investor interest should push yields down over the next year, at least in the London office market and at least by 25bps. The resulting increase in exit price will begin to make construction more viable, but in the medium term, the situation looks set to be one of shortage and increasing prices, assuming demand remains robust. This will continue to push rents for good-quality stock upwards, further supporting viability. This will take time to fix, though, meaning the whole issue of refurbishment and ‘retrofix’ moves up the agenda again as demand returns.

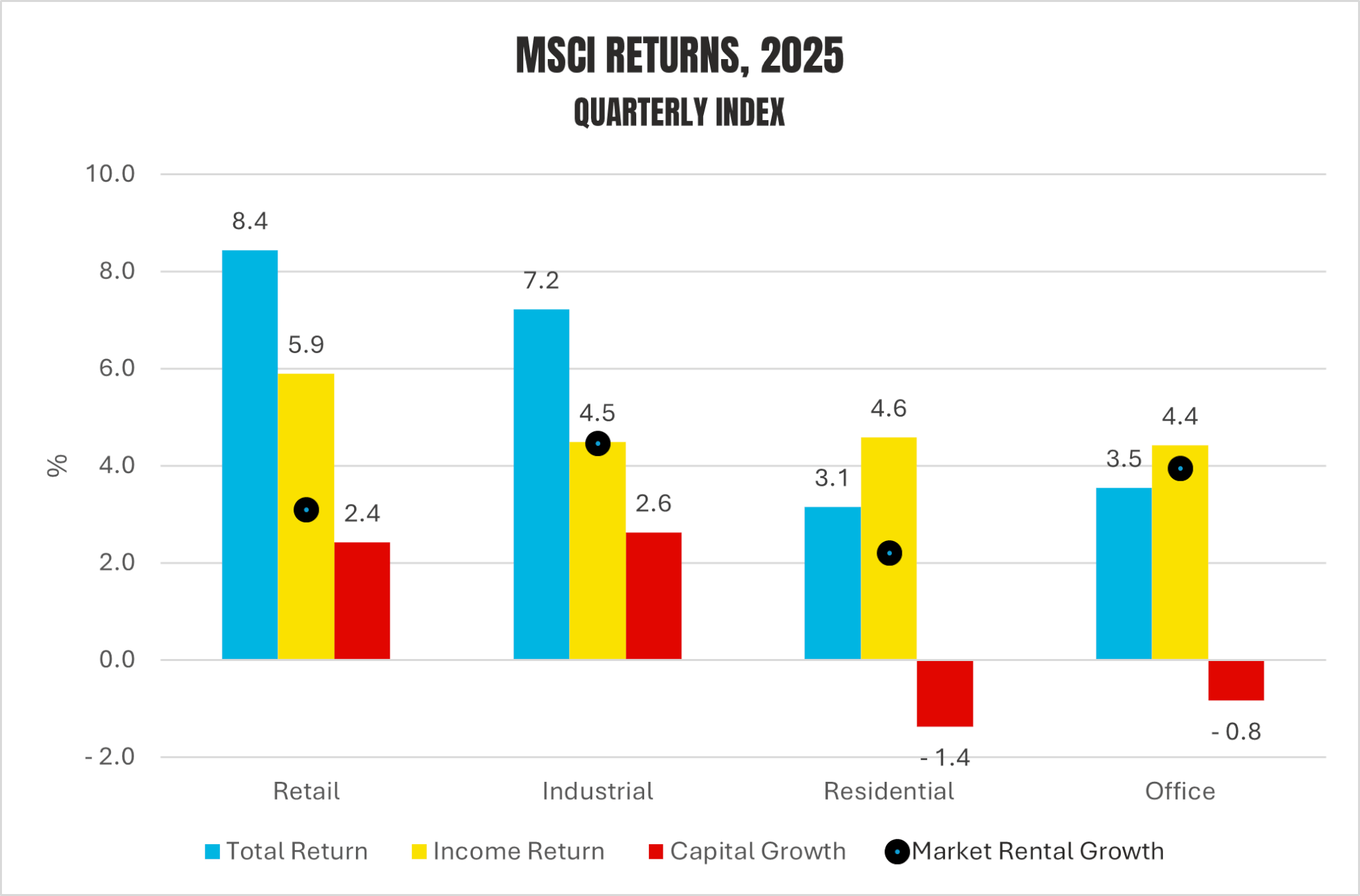

Looking at the MSCI performance data, though, retail saw the strongest returns in 2025 – 8.4%, driven mainly by very strong income returns (5.9%). As outlined above, retail spending is buoyant, and the flatness in internet sales proportions has confirmed that bricks-and-mortar shops have a future. The sector is now seeing rental and capital value growth, too – although all from the low base produced by the long years in the wilderness.

Source: MSCI

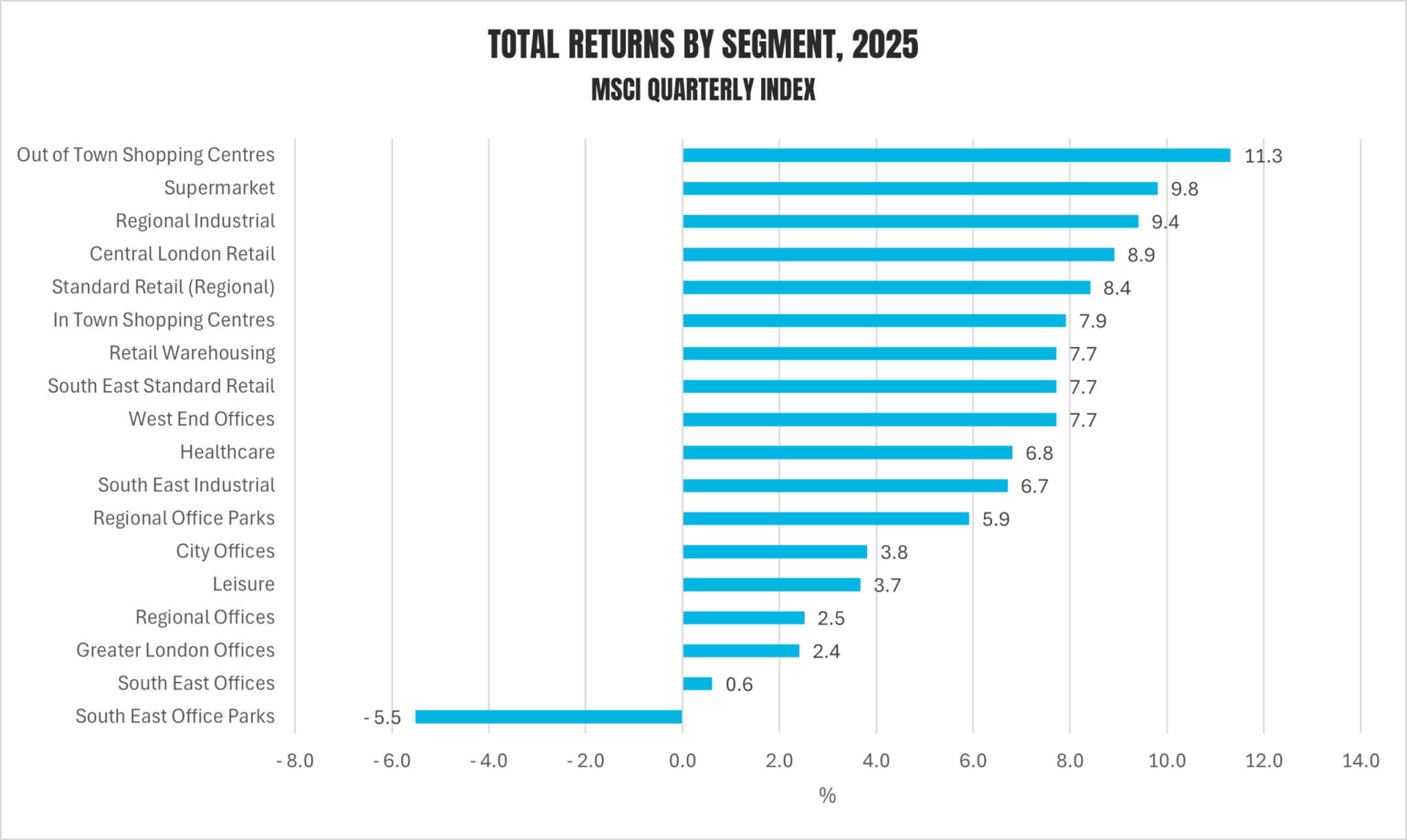

Of course, retail warehousing, supermarkets and out-of-town shopping centres have been doing well for a while, but the difference now is that they are joined by standard regional retail (8.4%) and Central London retail (8.9%). The weakness in investment may be more to do with a lack of supply, with investors perhaps choosing to hold onto such strongly income-producing stock.

Offices, on the other hand, remain highly polarised with West End offices’ total returns at 7.7%, and South East office parks at -5.5%. The urbanisation of office demand, particularly in the South, continues.

Source: MSCI

Source: MSCI

Residential Steadily Strengthening

Despite weak returns, residential is still seeing high volumes, though a number of large senior living transactions in Q4 skew the figures slightly; activity in the BTR sector slowed slightly towards the end of the year. However, there has been a resurgence in interest from investors, with a flurry of deals in London. At the end of 2025, M&G announced a joint venture with NPS, the Korean pension fund, to invest up to £1bn in UK multifamily, and other funds are gearing up for action. Meanwhile, Notting Hill Genesis’s sale of its BTR arm is also attracting huge interest.

This reflects gradually improving conditions in the London residential sector (see our research here) alongside the huge long-term potential of the sector, given low construction, rising population and persistent housing undersupply.

Conditions in the residential market are no exception to the slow improvement rule. Mortgage rates for higher LTVs have come down by almost a percentage point over the past year, and look set to fall further; greater competition for borrowers will force down margins even as rates fall. The rental market will become increasingly constrained over the year as the supply of properties falls back, a result of the combination of recent low BTR activity and smaller-scale landlords continuing to exit the market.

At the moment, though, the North and Midlands look more buoyant in terms of pricing and activity across both sides of the market, a result, really, of housing taking up a smaller proportion of people’s pay. But the above factors will lead to a recovery in London, where affordability has been most challenged.

So, in summary, wherever we look, the market seems to have reached an inflexion point. Unless something dramatic happens, things should get better in most sectors from now on. Just don’t expect a boom, though.

If you have any questions about this briefing note or any other aspect of the commercial or residential market, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

Bottoming Out: Positioning for Recovery

Executive summary

- After years of record-low starts and collapsing activity, early signs indicate that the end of 2025 marked a genuine turning point in London’s housing market, with investor interest increasing and construction gaining pace.

- Given delivery lags, completions in both BTS and multifamily BTR are set to fall sharply in 2027–28, tightening availability and pushing up rents, sales values and demand for sites.

- With viability improving and this supply squeeze on the horizon, 2026 represents a rare window of opportunity for land acquisition and alternative-use housing strategies for institutional capital.

Year-End 2025: UK Autumn Budget, Markets and Economy

CONTINUE TO THE PDF

As we close out 2025, the UK economy presents a complex picture: GDP growth has slowed, inflation is easing, and markets are adjusting to fiscal signals from the Autumn Budget. Beneath the headlines, there are signs of resilience, particularly in Central London leasing and selective investor appetite in industrial and residential sectors.

Our latest report provides a comprehensive review, including:

- Autumn Budget Analysis – Policy changes and their implications for growth and viability

- Markets Overview – Office and industrial leasing patterns, residential delivery challenges, and regional contrasts

- The Wider Economic Backdrop – GDP trends, inflation forecasts, and gilt yield movements

Click the link to read the complete PDF update. If you have any questions about this briefing note, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments – learn more here.

Executive Summary

ACCESS THE RESEARCH

Britain’s cities have undergone a remarkable reinvention over recent decades. Once characterised by derelict Victoriana or post-war concrete, many urban centres have been reshaped through large-scale transformative projects, this report’s definition of regeneration.

Heritage buildings have been repurposed; new quarters provided with high-quality public space, anchored by cultural institutions; and city living has become mainstream. These efforts have helped turn such locations into vibrant destinations that attract investment.

But this transformation is uneven and fragile. Gleaming new buildings sit cheek-by-jowl with obsolescent, empty buildings and deprived enclaves, while local authority budgets are under extreme pressure.

Cities and towns have ambitious plans to continue to address these problems. But since the pandemic, rising construction and debt costs, stalled projects, and slowing demand have undermined progress. The sense is growing that Britain’s urban fabric is beginning to fray.

Nevertheless, there is optimism – and not without reason. Some projects are making progress despite the headwinds; others are creating inventive frameworks and approaches to enable it in the future. This report explores the state of regeneration across the UK – and the future of it – by drawing on:

- Site visits to eight major regeneration projects – Elephant Park, Old Oak Common, Royal Albert Dock (London), Bradford, Dundee, Liverpool, Brabazon in Filton near Bristol, and Harlow.

- Interviews with practitioners and stakeholders directly engaged in delivering, financing, and planning regeneration.

Together, these sources provide a grounded picture: the old regeneration models no longer work, and a new approach needs to emerge.

This report provides insight into the complex problems surrounding urban regeneration across the UK. For investors, developers, and local authorities, this is not just analysis – it’s a roadmap for action. We highlight where opportunities lie and how you can position yourself to drive the next phase of regeneration.

Based on visits to the eight ongoing projects and interviews with those involved, we aim to unlock value from those complex challenges and opportunities and offer actionable insight. While the picture is sometimes a little bleak, there are also plenty of new ideas and reasons for optimism.

Historic Models No Longer Work

Past phases of regeneration were shaped by their time. The 1980s saw bold public sector intervention through Urban Development Corporations; the 1990s and 2000s leaned heavily on private investment during years of growth; the 2010s were defined by austerity, competitive bidding pots, and a patchwork of “levelling up” programmes focused on “left behind” towns.

These models are now exhausted. The combination of elevated costs, tighter regulation, weaker public capacity, and more cautious private capital means the formulas that once delivered Canary Wharf or Manchester’s renaissance are no longer fit for purpose. A ‘fourth phase’ of regeneration, with a different modus operandi, is starting to take shape.

“The public sector is going to have to move up the risk curve and take a more active role in regeneration – similar to the eighties and nineties, but more locally led.” – Local Authority Head of Regeneration