London Housing Crisis

Carried out earlier this year, our London and South East Residential Land Survey comes at a time when the capital’s development market is in the spotlight.

According to National Statistics, just 7,480 homes were started last year. This was up from the 6,600 started in 2024, but less than half the 10-year average of 16,000, and a fraction of the London Plan target of around 80,000 per annum. This is a national-scale crisis, given the capital’s importance to the UK economy.

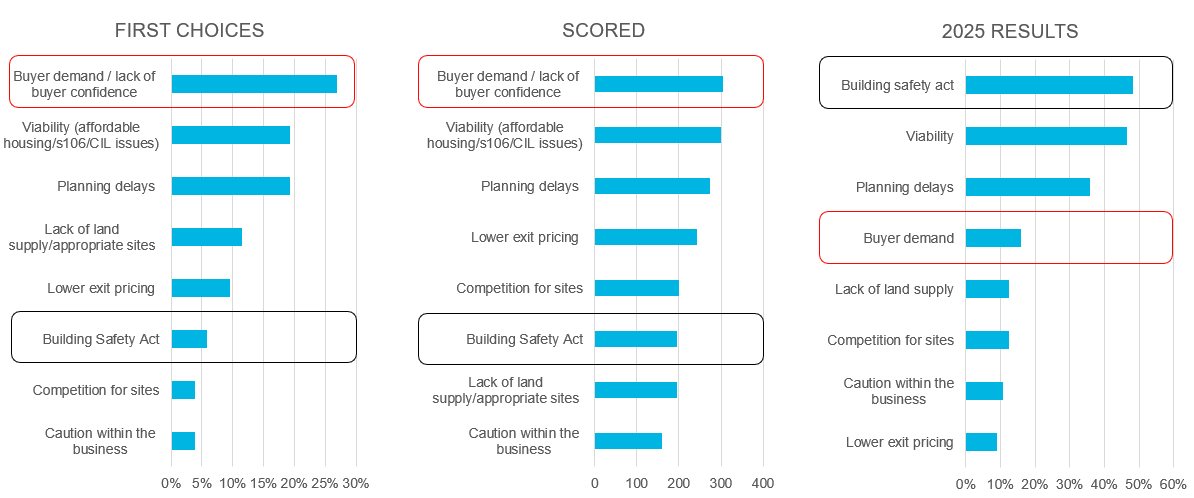

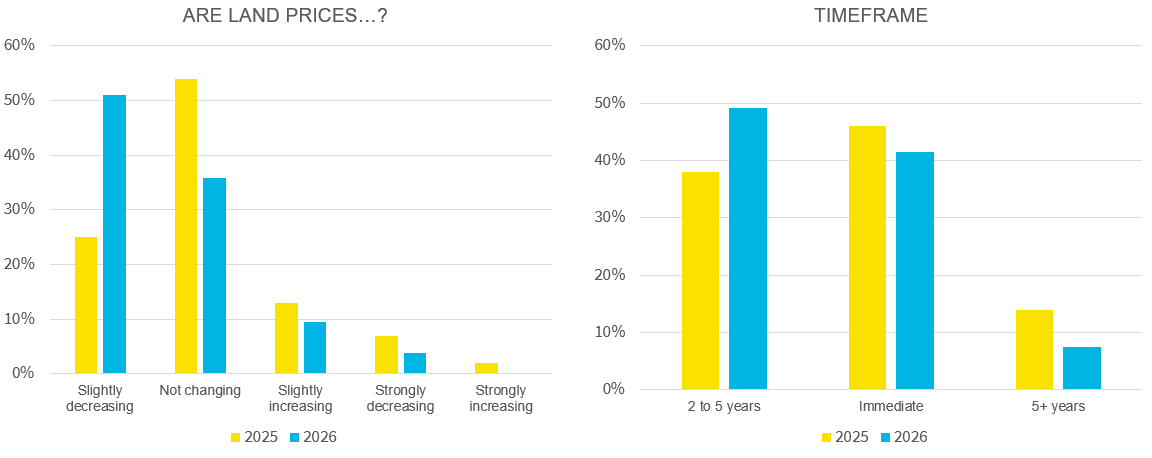

Part of the problem is the higher construction and debt costs of the past few years, but many have also pointed the finger at high costs for affordable housing and the Community Infrastructure Levy (CIL). Another major issue has been the slow progress of the Building Safety process introduced by the 2022 Building Safety Act, particularly the ‘Gateway 2’ step. In our 2025 survey, 48% of people attributed delays to this process, with viability close behind at 46%.

But this year’s results, covering 53 developers and investors, show a different pattern.