Market Pulse: Geopolitical Shocks Delay Recovery as Markets Remain Resilient

Download PDF

29 May, 2026 · 7 min read

Back in early February, it seemed as if things might finally be looking up for the property market.

Firstly, inflation was clearly on the way down. That meant the Bank of England would be able to cut rates by 50bps or even 75bps over 2026, and gilt and swap rates would fall (albeit not at the same pace).

Lower risk-free rates would make existing property pricing look more attractive to buyers, while debt was set to become accretive again as costs fell.

Secondly, the economy – while hardly looking like it was entering boom territory – appeared to be on the verge of a fragile and gradual recovery, driven by lower inflation and falling energy costs.

Finally, many occupier markets were seeing some reversal in fortunes. Industrial leasing appeared to have bottomed out and was increasing; regional offices were showing some signs of life; and residential development starts were trending upwards, albeit from an unprecedentedly low base.

In turn, investors were responding. Total volumes in Q4 reached £20.4bn, the highest total for almost three years. All segments were seeing an upward tick in activity, but it was most notable for the residential market. Build-to-rent investors appeared to have returned, while confidence was building in offices, in Central London in particular.

And then, on February 28th, the United States began “Operation Epic Fury” with a string of missile strikes on Iran and the assassination of the regime’s Supreme Leader. In response, Iran attacked the US’s Gulf allies and effectively closed the Strait of Hormuz.

The Strait is one of the world’s most important shipping lanes. It carries about 20-25% of the world’s oil exports and about 20% of its LNG exports. While the UK and Europe are less dependent on Strait-carried oil than Asia – although they are affected too through global pricing and shortages of some refined products – the gas element is potentially more important, especially for the UK.

Brent Crude prices rose from around $60 to over $100 and have remained volatile given the level of uncertainty over the future of the conflict. Meanwhile, European gas prices jumped by around 70% in the days after the war and have since fallen back to around 50% above pre-conflict levels.

While these are huge jumps, it is important to emphasise that it is much more modest than the shock that occurred after Russia’s invasion of Ukraine in 2022.

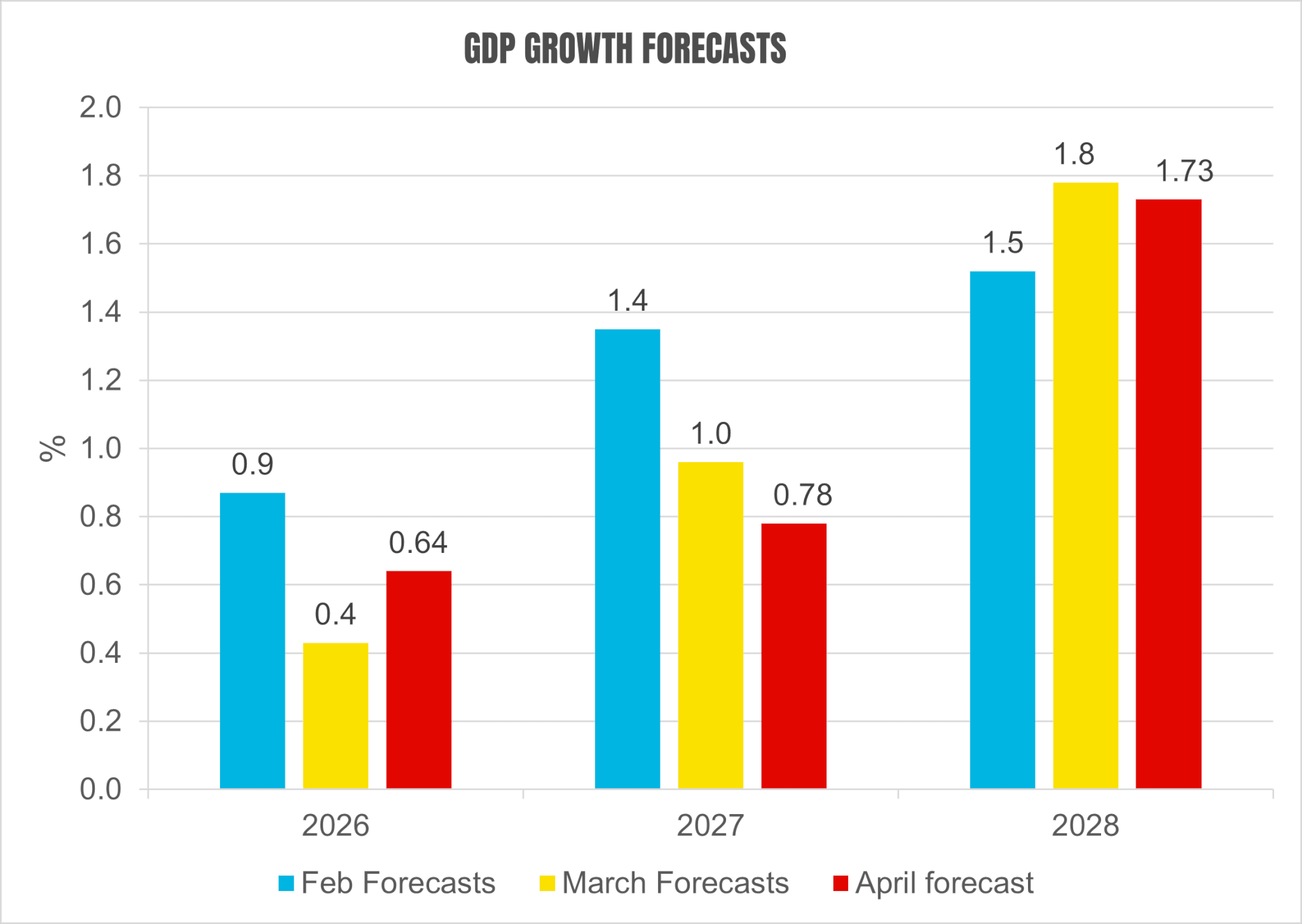

This will all weigh on the economy, as it will increase costs for both business and households and reduce investment and consumption compared to expectations. Oxford Economics has cut its forecasts for 2026 from 0.9% in January to 0.6% in April.

Source: Oxford Economics

The April forecast for 2026 has been tweaked upwards slightly as a result of strong outturns in the year so far. However, the 2027 forecast was reduced from 1.4% in February to 1.0% in March, and then taken down another 20bps to 0.8% in April.

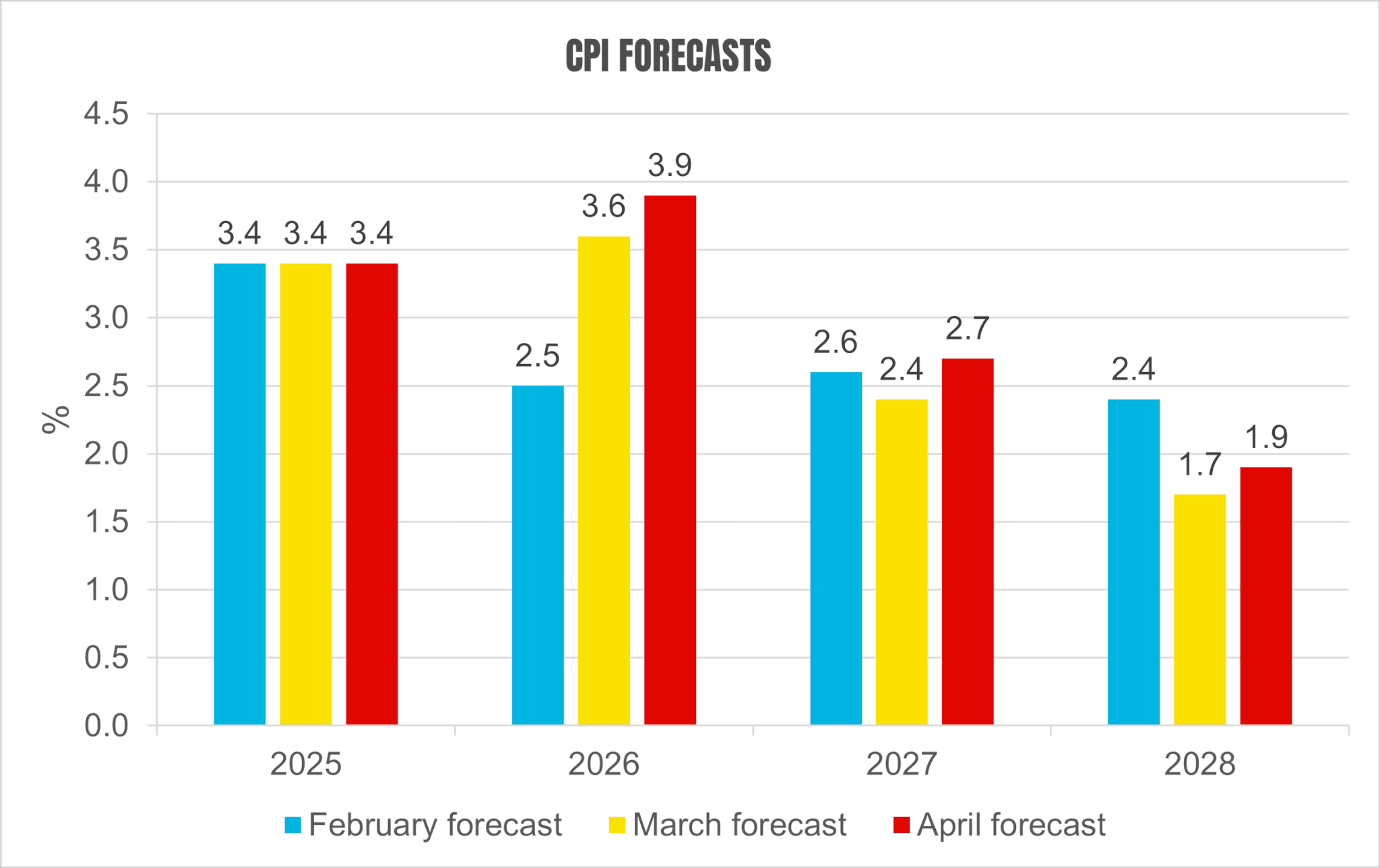

This is obviously serious, but the more dramatic impacts have been on inflation expectations. Annual change in CPI was trending downwards in the second half of last year, with forecasts pointing towards 2.5% by the end of 2026.

This would give the Bank of England room to cut base rates, with two or even three 25bps slated at that point for the year ahead.

But Oxford’s forecasts for CPI in March, in the wake of Iran, saw that rise to 3.6% – a figure that was subsequently adjusted upwards to 3.9%. This is partly a result of the direct impact of higher energy costs, but also the indirect effects on goods through increased transport and materials costs (oil and gas are important feedstocks for some manufactured goods).

Source: Oxford Economics

The Monetary Policy Committee (MPC) will be very aware of these potential “second-order” costs, particularly if they shift consumers’ price expectations. This would lead to demands for higher wages and a potential wage-price spiral. The MPC has been criticised for failing to act quickly enough after the energy shock caused by the Ukraine war, so it will be keen not to make the same mistake again.

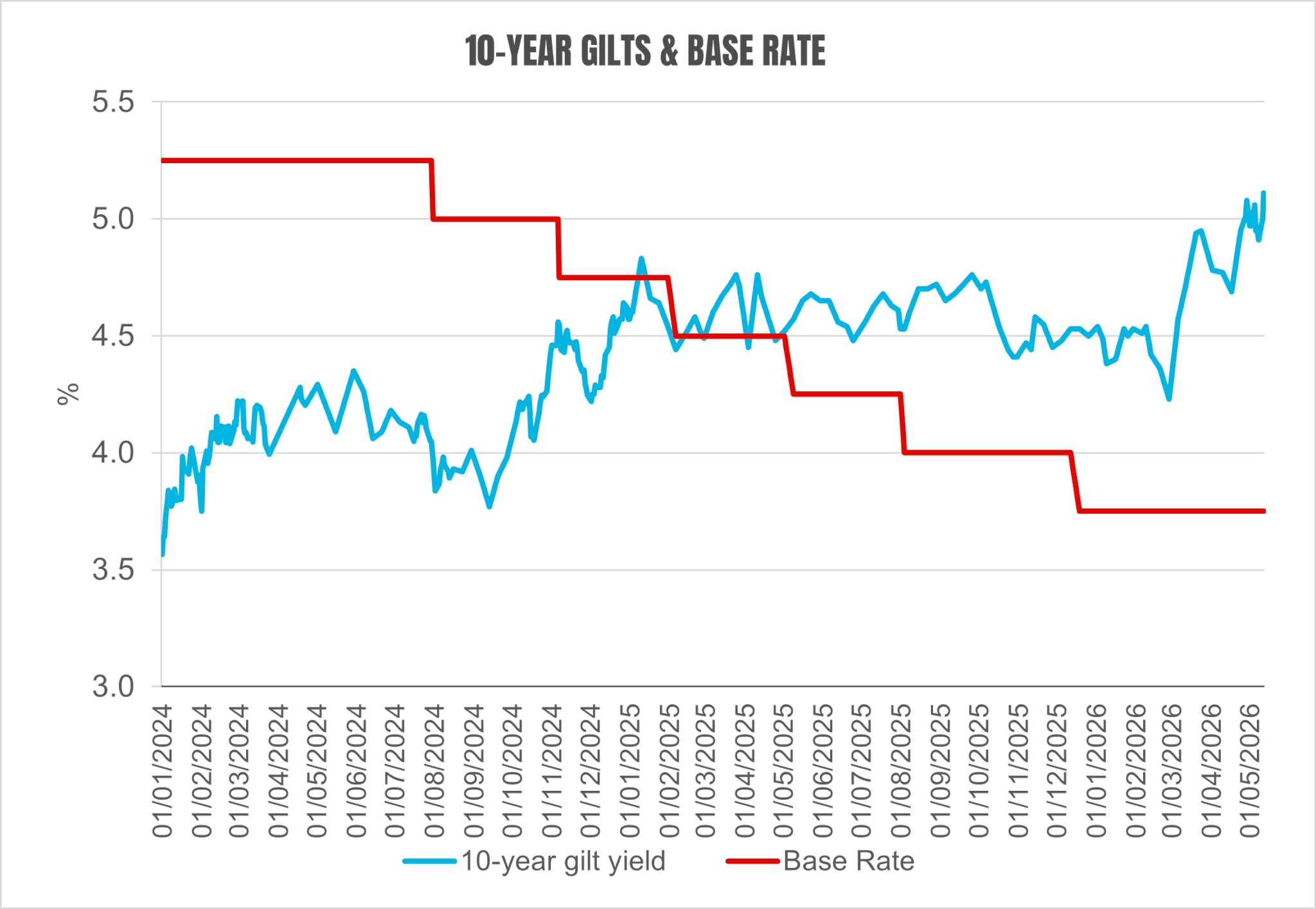

Higher inflation means that bond investors will demand more in interest to compensate for that erosion in value. But there’s more: slower economic growth points to lower tax revenue, which further casts doubt on the UK government’s fiscal sustainability – an issue which was already of concern to bondholders.

The resulting “sell-off” of this government debt led to an increase in supply and a reduction in demand – meaning a fall in price, or a rise in yields as they move in opposite directions.

The local elections have added further uncertainty to this picture. A Labour leadership contest is looking increasingly likely, and bond investors will be concerned that Keir Starmer will be replaced by a leader with a higher-borrowing, higher-spending instincts. This has added another risk premium to gilts.

Source: Bank of England / MarketWatch

The problem for property is that 10-year gilts often represent the “risk-free rate” against which fair value is calculated. The greater confidence in the market at the beginning of the year was due to the anticipation that yields would start moving downwards. Not only would that make it easier for buyers to meet vendor expectations around pricing, but it would also give them the confidence that their property would be worth more in the years ahead.

That expectation has been, to put it bluntly, shattered, at least in the short to medium term. The hike in bond yields suggests that property yields will, at best, stay where they are – at least in aggregate (some sectors are more insulated than others, see below).

This suggests that the increase in transaction volumes seen at the end of last year will not be sustained. And indeed, volumes in Q1 2026 came in at £9.0bn, the lowest total since Q3 2023. All sectors were hit, except residential, which continued the strong activity it saw in Q4.

To be fair, it is unclear whether this is a direct result of the Iran war, which after all, broke out at the end of February, but March tends to be the strongest of the three months for deals.

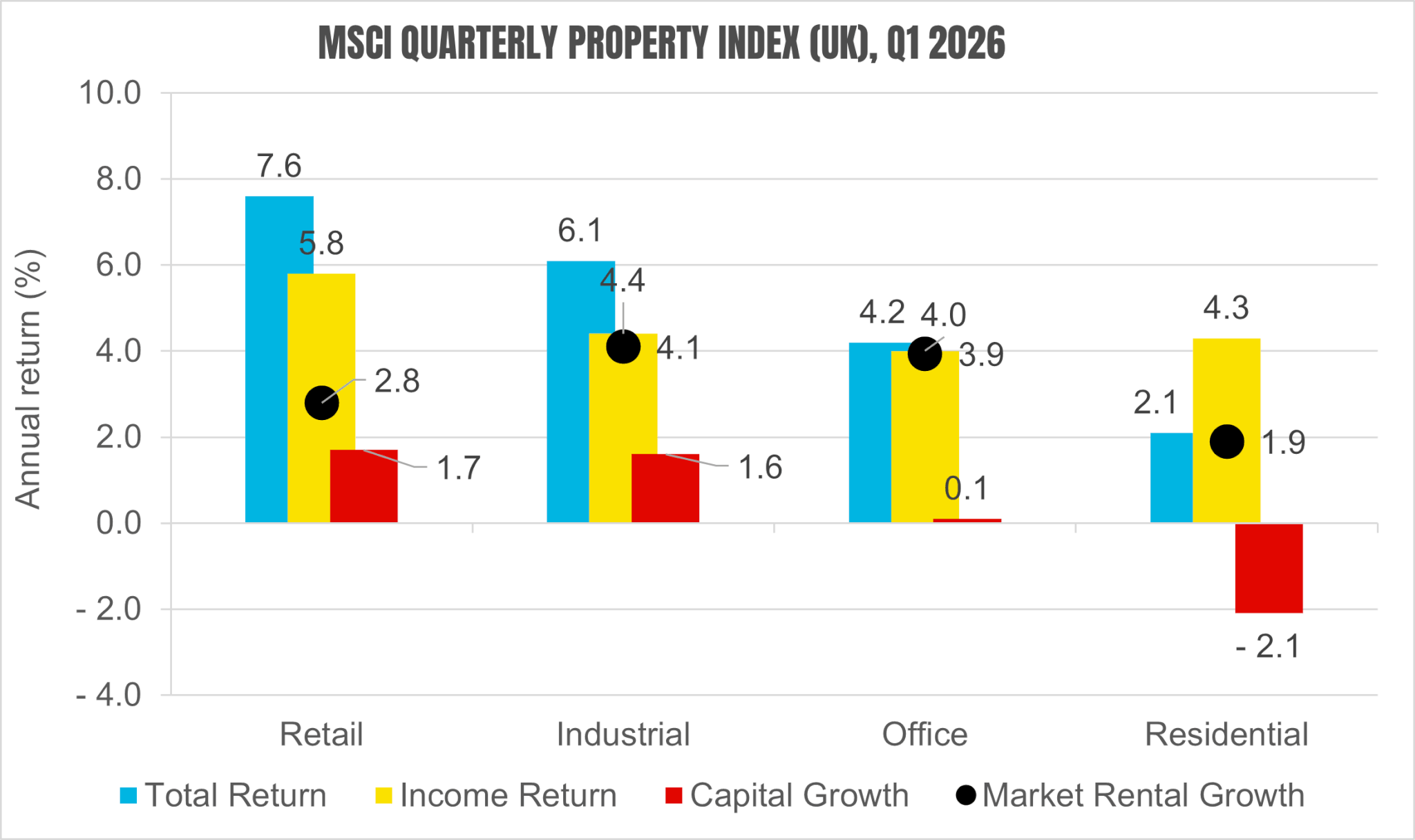

MSCI Total Returns slipped back for retail and industrial, from 8.4% to 7.6% and from 7.2% to 6.1% respectively. This was driven by a sharp fall in capital growth. Residential saw a similar slippage despite the interest, from 3.1% to 2.1%, with negative capital growth intensifying from -1.4% to -2.1%.

Offices, however, moved in the other direction; capital values are now flat year-on-year (compared to -1.4% at Q4), and this has pushed total returns up by 70bps to 4.2%. Yields in some office segments had reached quite high levels and are presumably less affected by the shifts in bond yields, and in some areas, confidence is returning to the market more generally. The fact that the West End is seen as a safe haven for wealth preservation is another factor.

Source: MSCI

Some of this may reflect base effects – there was quite a lot of capital growth back in Q1 2025, but more modest figures for the rest of the year. This historic growth has fallen out of the figures for this quarter, making the shift to weaker growth look more recent than it is. But it is also an indication that the war is beginning to have an impact on pricing and confidence.

The leasing market was more robust. Across both office and industrial markets, leasing remained in line with the long-term average, with vacancy generally now on a falling trend. This should prevent sentiment and rental growth from deteriorating rapidly.

The residential market is likely to be most affected by the war in Iran. Investment will be subject to the same forces as elsewhere in the property market, but it has the additional issue of the mortgage market. Shortly after the war broke out, thousands of mortgage products were removed from the market, and average rates, which had been strongly trending down since the start of 2025, have now risen by 50-100bps depending on length and LTV.

This will clearly impact the demand for property, further reducing developers’ ability to build much-needed homes. Viability for such development will also be impacted by higher debt costs and materials costs (as it will across other sectors). This will not have an equal effect on all development types, as material mixes will differ.

There is a brighter outlook for one part of residential, though. RICS surveys indicate increasing unsold stock among agents and decreasing sales and enquiries, but the rental market is going in the opposite direction. Stock is decreasing and tenant demand is increasing.

This is perhaps unsurprising, as some people who can’t (or won’t) buy at the moment are forced into renting. Meanwhile, there is some evidence that the stock of rental property is reducing as landlords exit the market, as a result of the cumulative effect of legislation, as well as the upcoming Renters’ Rights Act.

Together, this suggests that rents – which have been flat for the past year to 18 months – may begin to rise again. Investors have been attracted to the sector not by the short-term dynamics, which have been difficult given costs and yields, but by the long-term demographic tailwinds, structural shortages and portfolio diversification benefits. Rising rents could ensure that, despite all the issues elsewhere, it remains the target of investor interest.

Industrial – still fashionable globally with investors – and central London, where activity continues apace amid a shortage of new good quality stock, also look resilient.

The market is likely to, at best, remain weak over the next quarter or two. The course of the war and the blockades are uncertain– as is the degree to which the economy is impacted. The drama within the Labour Party adds a further negative factor.

The most recent GDP figures, out at the time of writing, show a 0.6% expansion in Q1, with GDP per capita rising by a similar amount. There are suspicions that this is a statistical illusion, but there are some other indications, such as retail sales and the PMIs, that growth is more robust than feared.

It is early days in terms of the impact of the energy shock and any leadership contest, of course, and economic prospects have certainly weakened. But the big unknown is to what extent, and how that impacts the property market.

In conclusion, the recovery has been delayed but not necessarily derailed. Pricing will be under pressure, but the leasing market looks generally robust, particularly in London offices. And while the residential sales market is likely to struggle, the rental side may gradually recover, if only because of a shortage of supply.

If you have any questions about this briefing note or any other aspect of the commercial or residential market, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

Download PDF