Inflation Falls, Investment Rises and Key Sectors Begin to Recover

Note: This briefing was finalised on 23 February, before recent events in Iran and the wider Middle East. Energy prices have spiked, and there are concerns that this could lead to higher inflation, slowing down the speed of future base rate cuts and, in turn, the speed of the gradual recovery outlined below. Much will depend on the length of the conflict and the resulting disruption to oil and gas supplies.

Overview

- The UK economy is showing signs of a gradual improvement. While growth is set to remain modest, inflation is easing, and interest rates are falling. This will provide a more supportive backdrop for markets as 2026 unfolds.

- Property markets – and the sentiment around them – appear to have reached an inflexion point. Investment volumes saw the strongest activity in four years in the fourth quarter, led by offices and industrial. This momentum looks set to be sustained, although it will be a gradual improvement, not a boom.

- Across offices, industrial and residential, low construction and robust demand will push up rents over the year, gradually easing viability challenges – although it will be some time before supply can recover more strongly.

A Gradually Improving Economic Backdrop

The final economic reading of the year, GDP growth in Q4, came in with a lacklustre 0.1%, but over 2025, the UK economy grew by 1.3%. This is clearly not spectacular, but it is not terrible either – which might come as a surprise given the economic doom and gloom in the press. Even GDP per capita rose by 1.0% over the year, up from a big fat zero in 2024.

This kind of story is repeated across lots of datasets in both property markets and the wider economy. Slowly, things are beginning to improve, albeit usually at an unimpressive rate. But the results should be more apparent as 2026 progresses.

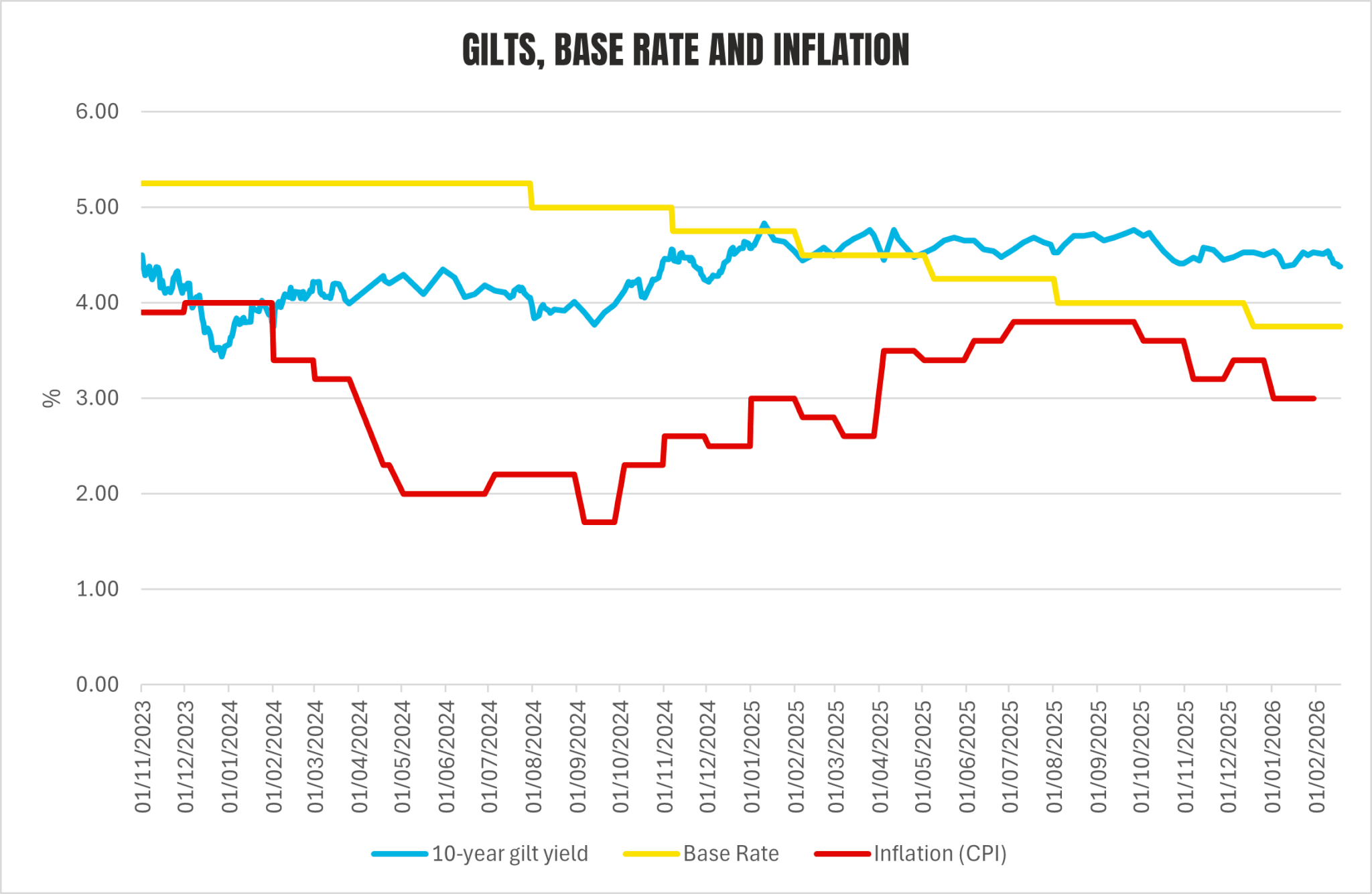

Take inflation as measured by CPI. December’s outturn was a little disappointing – 3.4%, up from 3.2% in November and slightly ahead of market expectations. But January saw it fall to 3.0%. Since the Summer peak, the trend has been clearly downwards. This is evident in the labour market, which is becoming looser; redundancies are increasing, vacancies are decreasing, and private sector wage growth is slowing.

The Bank of England had adopted a slow and cautious approach to cuts, with forecasters expecting just another two 25bps cuts over 2026, bringing the base rate to 3.25% by year-end. But it’s entirely possible that if all these measures continue trending downwards, there is another 25bps by year-end.

The slightly better economy is, of course, related to falling inflation and interest rates as well as the surprising fact that business investment has been running at historic highs since the pandemic (presumably related to technology). Oxford Economics is forecasting a slightly gloomier GDP growth of just 0.9% in 2026, but this may well be overshot if the wider context continues improving.

10-year gilts, the ‘risk-free rate’ against which property returns are compared, are a slightly different story. The bond market is not only reacting somewhat slower to changes – reflecting the scale of government borrowing both domestically and internationally – it is more volatile. This reflects the UK’s fragility, not just its own poor finances but also the vulnerable position of Kier Starmer and Rachel Reeves. Their replacement with a less fiscally conservative pairing is clearly a risk. At the time of writing, there are also rumours – indications, even – of further ‘events’ in the Middle East, which would also upset the wider picture.

Source: Bank of England + National Statistics + Market Watch

Assuming that none of this derails things too much, then bond yields should follow their choppy path downwards, with the result that property yields gradually become more appealing. Indeed, there is some evidence that the combination of solid if uninspiring growth, reducing rates and strengthening fundamentals in some markets has already been enough to get the market moving again.

Market Conditions Reaching an Inflexion Point

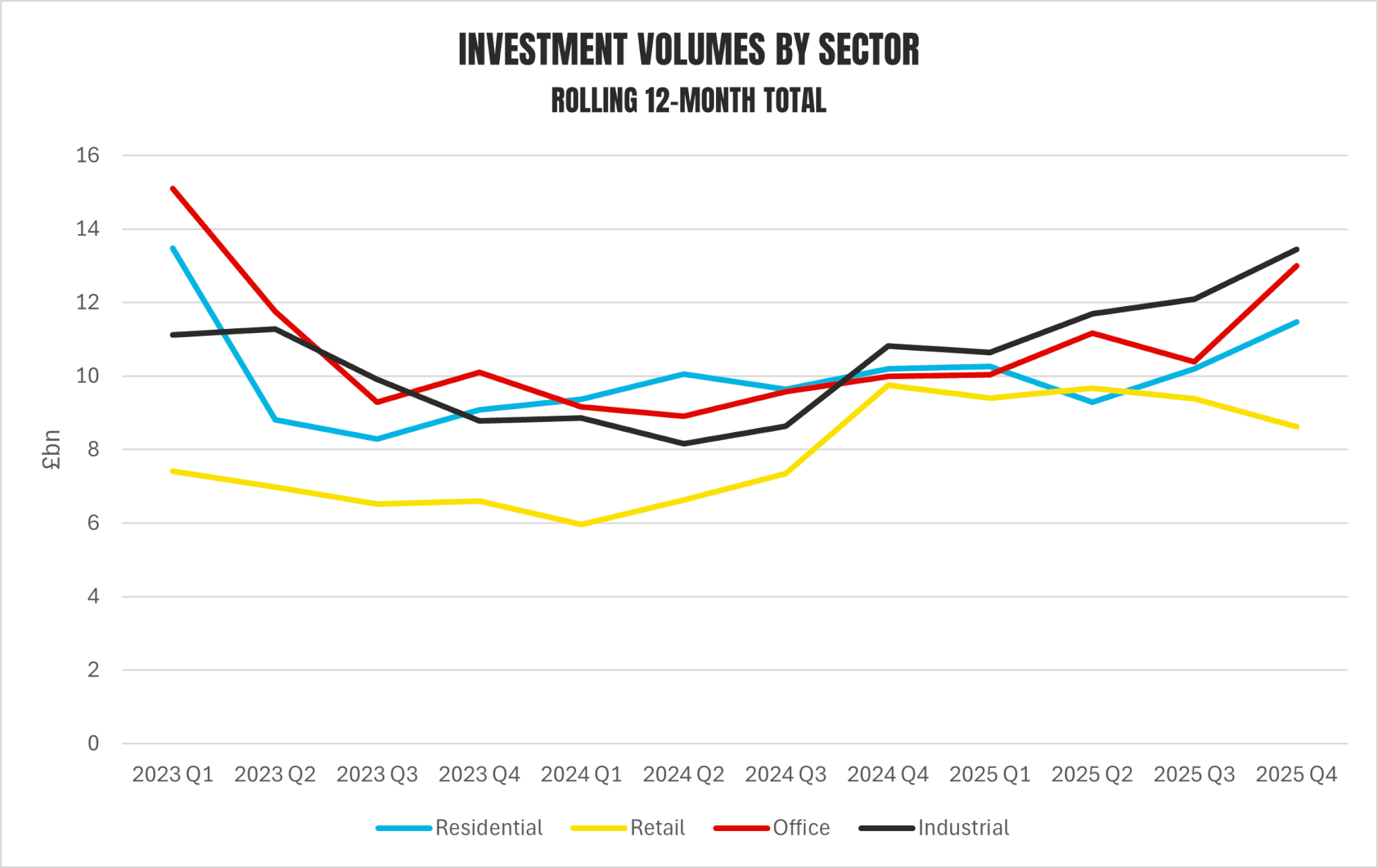

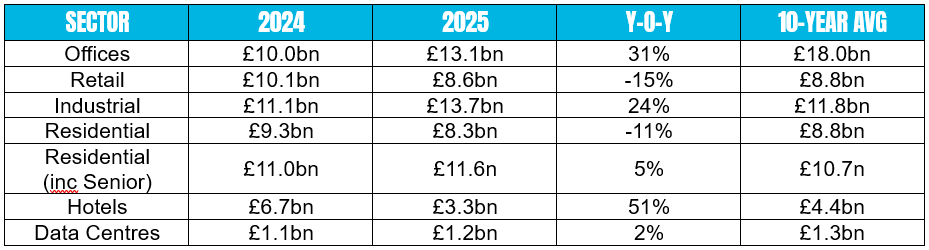

The final quarter of the year saw £17.1bn transacted, the highest total for almost four years. As can be seen below, every sector except retail is now seeing a steady upward trend. The standout was undoubtedly offices, which, with £6bn changing hands, saw the highest total since 2021. This was driven by some large-scale deals in London, with some major international institutions (Hines, Royal London) re-entering the fray.

Source: MSCI

The strong fundamentals in London’s office market have been apparent for a while. Rental growth has been strong, with prime city rents now at circa £100psf, compared to say £75psf three years ago. High vacancy rates obscure the shortage of new, high-quality offices that occupiers increasingly crave. Prelets have increased as businesses have looked to the pipeline, rather than the increasingly obsolescent-looking existing stock.

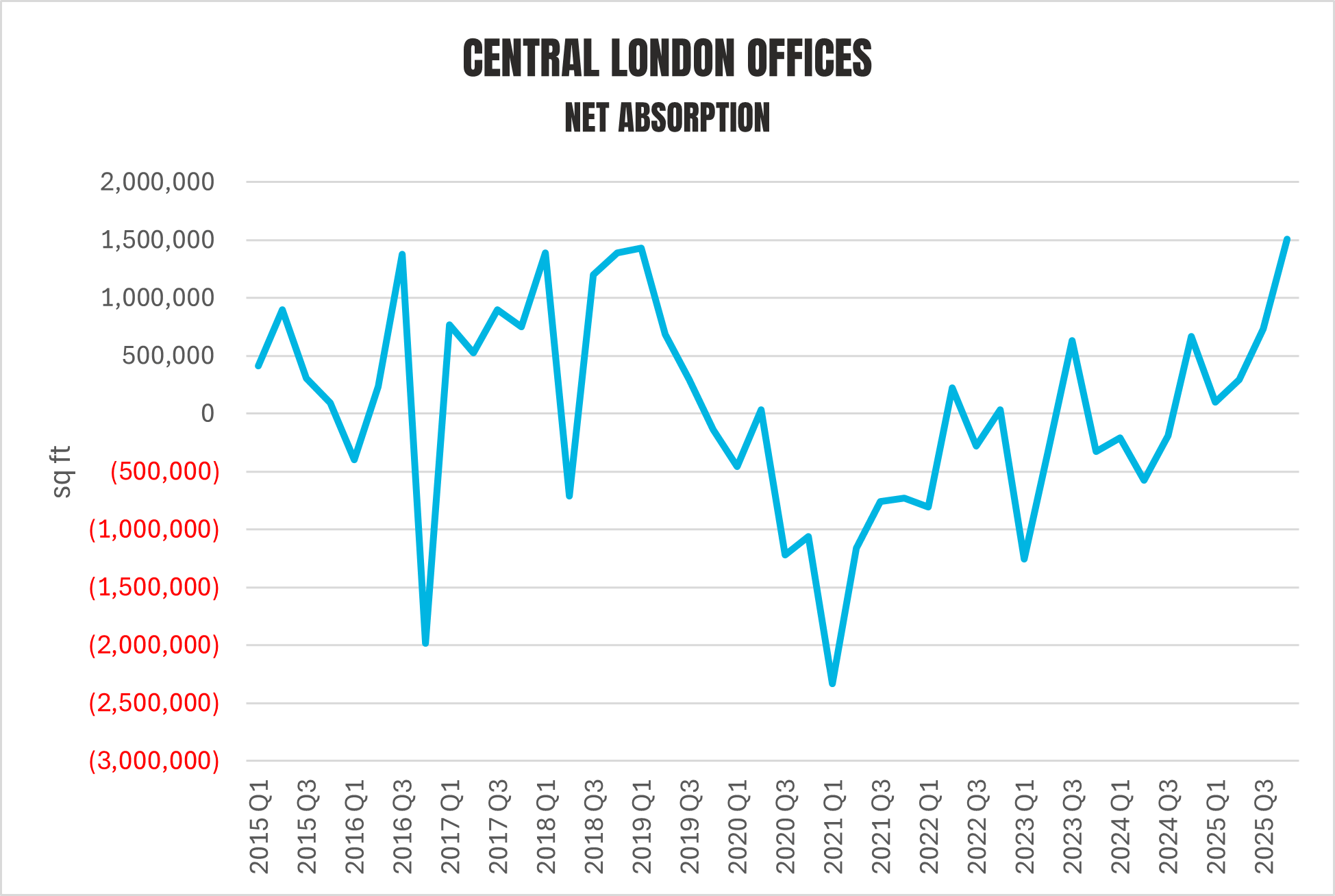

Net absorption in the Central London market was at its highest on record, even though leasing fell back, suggesting that companies are simply becoming less minded to leave space given constrained availability. Meanwhile, space under construction and construction starts are lower than they were a year ago. But most importantly, investor sentiment has turned, and even if you are sceptical about the arguments around polarisation, the herding effect alone should see both values and volumes rise over 2026.

Source: CoStar

The situation is, if anything, even more stark in the major cities outside London. There have been practically zero starts in every ‘big six’ city except one, and vanishingly small amounts under construction. Manchester stands out as the exception, with 400,000 sq ft started over the past twelve months. It is true that this city had the highest take-up over 2025, but it is not so far ahead of the pack to justify such an incongruity. I do wonder if some of the recent hype over its economy is skewing investment. Now that’s not to say it is doing well – it very clearly is, as any time spent in the city will confirm – but there are some questions over whether the very high figures for productivity growth (see here) are accurate.

Diverging Sector Performance

Industrial, on the other hand, is still seeing very strong investment, albeit not the great jump upwards seen by offices. The total for 2025, at £11.1bn, was the highest of any sector (just), and represented a 24% increase on 2024. I’ve had mild concerns about industrial for a while; leasing has been muted for two years or so, while vacancy has been rising, and rental growth has slowed considerably.

But over the last few months, a corner has been turned. The pattern is similar to the London office market – falling vacancy and increasing net absorption amid lower leasing activity. This implies that companies are simply not moving because there is insufficient new, good-quality space. (The main difference, though, is that the standout region now is the North-West).

Source: MSCI

So, in offices, residential and industrial, in some locations at least, the market is effectively screaming ‘build’. But that is more easily said than done. Construction costs and development debt costs remain high. Moreover, yields have not yet really budged downwards, partly a result of what’s happening in the gilt market.

The increase in investor interest should push yields down over the next year, at least in the London office market and at least by 25bps. The resulting increase in exit price will begin to make construction more viable, but in the medium term, the situation looks set to be one of shortage and increasing prices, assuming demand remains robust. This will continue to push rents for good-quality stock upwards, further supporting viability. This will take time to fix, though, meaning the whole issue of refurbishment and ‘retrofix’ moves up the agenda again as demand returns.

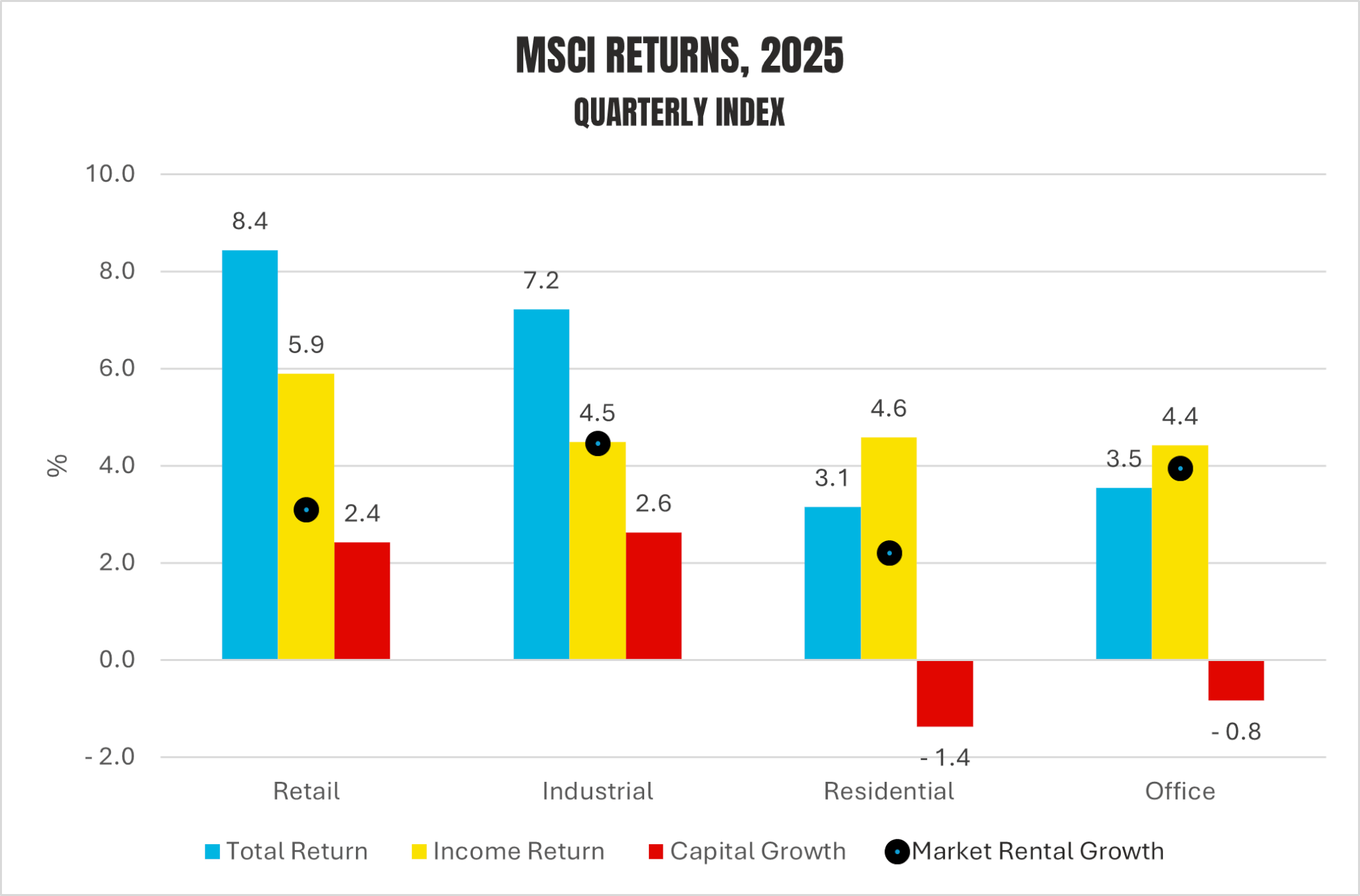

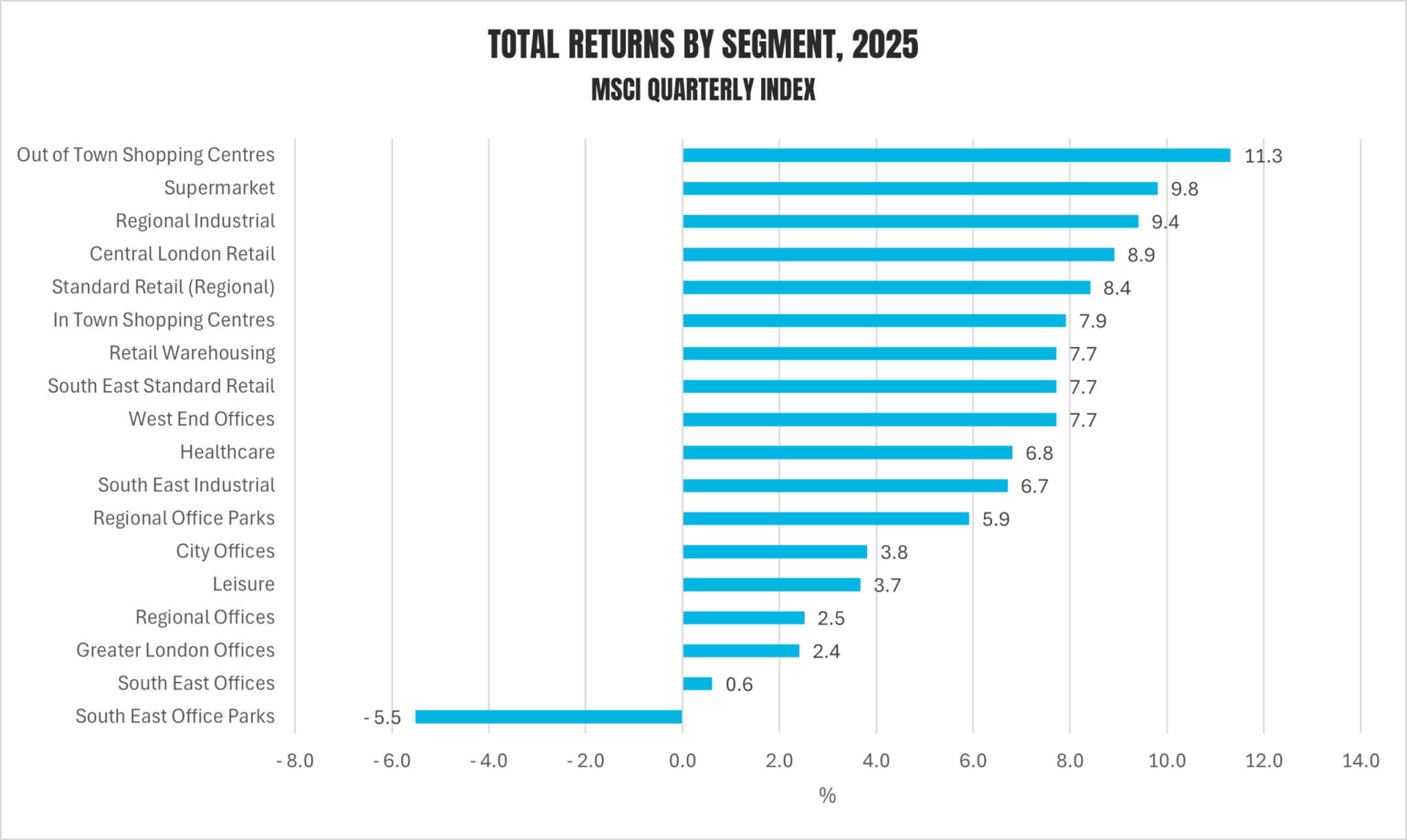

Looking at the MSCI performance data, though, retail saw the strongest returns in 2025 – 8.4%, driven mainly by very strong income returns (5.9%). As outlined above, retail spending is buoyant, and the flatness in internet sales proportions has confirmed that bricks-and-mortar shops have a future. The sector is now seeing rental and capital value growth, too – although all from the low base produced by the long years in the wilderness.

Source: MSCI

Of course, retail warehousing, supermarkets and out-of-town shopping centres have been doing well for a while, but the difference now is that they are joined by standard regional retail (8.4%) and Central London retail (8.9%). The weakness in investment may be more to do with a lack of supply, with investors perhaps choosing to hold onto such strongly income-producing stock.

Offices, on the other hand, remain highly polarised with West End offices’ total returns at 7.7%, and South East office parks at -5.5%. The urbanisation of office demand, particularly in the South, continues.

Source: MSCI

Source: MSCI

Residential Steadily Strengthening

Despite weak returns, residential is still seeing high volumes, though a number of large senior living transactions in Q4 skew the figures slightly; activity in the BTR sector slowed slightly towards the end of the year. However, there has been a resurgence in interest from investors, with a flurry of deals in London. At the end of 2025, M&G announced a joint venture with NPS, the Korean pension fund, to invest up to £1bn in UK multifamily, and other funds are gearing up for action. Meanwhile, Notting Hill Genesis’s sale of its BTR arm is also attracting huge interest.

This reflects gradually improving conditions in the London residential sector (see our research here) alongside the huge long-term potential of the sector, given low construction, rising population and persistent housing undersupply.

Conditions in the residential market are no exception to the slow improvement rule. Mortgage rates for higher LTVs have come down by almost a percentage point over the past year, and look set to fall further; greater competition for borrowers will force down margins even as rates fall. The rental market will become increasingly constrained over the year as the supply of properties falls back, a result of the combination of recent low BTR activity and smaller-scale landlords continuing to exit the market.

At the moment, though, the North and Midlands look more buoyant in terms of pricing and activity across both sides of the market, a result, really, of housing taking up a smaller proportion of people’s pay. But the above factors will lead to a recovery in London, where affordability has been most challenged.

So, in summary, wherever we look, the market seems to have reached an inflexion point. Unless something dramatic happens, things should get better in most sectors from now on. Just don’t expect a boom, though.

If you have any questions about this briefing note or any other aspect of the commercial or residential market, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

Bottoming Out: Positioning for Recovery

Executive summary

- After years of record-low starts and collapsing activity, early signs indicate that the end of 2025 marked a genuine turning point in London’s housing market, with investor interest increasing and construction gaining pace.

- Given delivery lags, completions in both BTS and multifamily BTR are set to fall sharply in 2027–28, tightening availability and pushing up rents, sales values and demand for sites.

- With viability improving and this supply squeeze on the horizon, 2026 represents a rare window of opportunity for land acquisition and alternative-use housing strategies for institutional capital.

Year-End 2025: UK Autumn Budget, Markets and Economy

CONTINUE TO THE PDF

As we close out 2025, the UK economy presents a complex picture: GDP growth has slowed, inflation is easing, and markets are adjusting to fiscal signals from the Autumn Budget. Beneath the headlines, there are signs of resilience, particularly in Central London leasing and selective investor appetite in industrial and residential sectors.

Our latest report provides a comprehensive review, including:

- Autumn Budget Analysis – Policy changes and their implications for growth and viability

- Markets Overview – Office and industrial leasing patterns, residential delivery challenges, and regional contrasts

- The Wider Economic Backdrop – GDP trends, inflation forecasts, and gilt yield movements

Click the link to read the complete PDF update. If you have any questions about this briefing note, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments – learn more here.

Executive Summary

ACCESS THE RESEARCH

Britain’s cities have undergone a remarkable reinvention over recent decades. Once characterised by derelict Victoriana or post-war concrete, many urban centres have been reshaped through large-scale transformative projects, this report’s definition of regeneration.

Heritage buildings have been repurposed; new quarters provided with high-quality public space, anchored by cultural institutions; and city living has become mainstream. These efforts have helped turn such locations into vibrant destinations that attract investment.

But this transformation is uneven and fragile. Gleaming new buildings sit cheek-by-jowl with obsolescent, empty buildings and deprived enclaves, while local authority budgets are under extreme pressure.

Cities and towns have ambitious plans to continue to address these problems. But since the pandemic, rising construction and debt costs, stalled projects, and slowing demand have undermined progress. The sense is growing that Britain’s urban fabric is beginning to fray.

Nevertheless, there is optimism – and not without reason. Some projects are making progress despite the headwinds; others are creating inventive frameworks and approaches to enable it in the future. This report explores the state of regeneration across the UK – and the future of it – by drawing on:

- Site visits to eight major regeneration projects – Elephant Park, Old Oak Common, Royal Albert Dock (London), Bradford, Dundee, Liverpool, Brabazon in Filton near Bristol, and Harlow.

- Interviews with practitioners and stakeholders directly engaged in delivering, financing, and planning regeneration.

Together, these sources provide a grounded picture: the old regeneration models no longer work, and a new approach needs to emerge.

This report provides insight into the complex problems surrounding urban regeneration across the UK. For investors, developers, and local authorities, this is not just analysis – it’s a roadmap for action. We highlight where opportunities lie and how you can position yourself to drive the next phase of regeneration.

Based on visits to the eight ongoing projects and interviews with those involved, we aim to unlock value from those complex challenges and opportunities and offer actionable insight. While the picture is sometimes a little bleak, there are also plenty of new ideas and reasons for optimism.

Historic Models No Longer Work

Past phases of regeneration were shaped by their time. The 1980s saw bold public sector intervention through Urban Development Corporations; the 1990s and 2000s leaned heavily on private investment during years of growth; the 2010s were defined by austerity, competitive bidding pots, and a patchwork of “levelling up” programmes focused on “left behind” towns.

These models are now exhausted. The combination of elevated costs, tighter regulation, weaker public capacity, and more cautious private capital means the formulas that once delivered Canary Wharf or Manchester’s renaissance are no longer fit for purpose. A ‘fourth phase’ of regeneration, with a different modus operandi, is starting to take shape.

“The public sector is going to have to move up the risk curve and take a more active role in regeneration – similar to the eighties and nineties, but more locally led.” – Local Authority Head of Regeneration

Full Report

Unlocking Urban Potential: The Next Phase of UK Regeneration

ACCESS THE RESEARCH

Britain’s cities have undergone a remarkable reinvention over recent decades. Once characterised by derelict Victoriana or post-war concrete, many urban centres have been reshaped through large-scale transformative projects, this report’s definition of regeneration.

Heritage buildings have been repurposed; new quarters provided with high-quality public space, anchored by cultural institutions; and city living has become mainstream. These efforts have helped turn such locations into vibrant destinations that attract investment.

But this transformation is uneven and fragile. Gleaming new buildings sit cheek-by-jowl with obsolescent, empty buildings and deprived enclaves, while local authority budgets are under extreme pressure.

Cities and towns have ambitious plans to continue to address these problems. But since the pandemic, rising construction and debt costs, stalled projects, and slowing demand have undermined progress. The sense is growing that Britain’s urban fabric is beginning to fray.

Nevertheless, there is optimism – and not without reason. Some projects are making progress despite the headwinds; others are creating inventive frameworks and approaches to enable it in the future. This report explores the state of regeneration across the UK – and the future of it – by drawing on:

Site visits to eight major regeneration projects – Elephant Park, Old Oak Common, Royal Albert Dock (London), Bradford, Dundee, Liverpool, Brabazon in Filton near Bristol, and Harlow.

- Interviews with practitioners and stakeholders directly engaged in delivering, financing, and planning regeneration.

- Together, these sources provide a grounded picture: the old regeneration models no longer work, and a new approach needs to emerge.

This research report provides insight into the complex problems surrounding urban regeneration across the UK. For investors, developers, and local authorities, this is not just analysis – it’s a roadmap for action. We highlight where opportunities lie and how you can position yourself to drive the next phase of regeneration.

Click HERE to read the complete research or explore the executive summary HERE. You can also contact Jon or the wider Montagu Evans team to discuss more.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

London’s Homebuilding Crisis: An Overview of the Research

2) OVERVIEW

Housing starts in London have collapsed: According to Molior, only 3,248 homes began construction over the first nine months of 2025, equivalent to just 11% of the recent average and under 5% of the government’s target. Affordable housing delivery has fallen back even more sharply.

This is a crisis with huge implications for the living standards of Londoners, the economy of the capital, and the robustness of its construction industry and supply chains. Given the city’s central role in both housing delivery and the national economy, it needs urgent attention at both central and local government levels.

What are the reasons for this collapse?

- Regulatory delays: Building Safety Act and Gateway processes have created bottlenecks, with only 9% of tall building applications approved since 2023.

- Viability challenges: Construction and debt costs have surged, while residential land values have dropped. Regulatory burdens and inflexible affordable housing quotas make schemes unprofitable. Land values are now not high enough to convince owners to sell, and in some cases are negative.

- Weak demand: Overseas investors have retreated, domestic buyers face affordability constraints, and unsold stock is building up. Prices have not fallen in response to lower demand as developers have tried to keep sites profitable. This is not giving the wider market the confidence to proceed.

- Affordable housing crisis: Grant funding is insufficient, quotas are too high, and Registered Providers lack the capacity to take on s106 units. As so many sites in London are mixed tenure and in flatted blocks, affordable housing is tied to private delivery more than elsewhere in the country.

- Market shift: Developers currently prefer lower-density suburban projects, which in London are prevented by green belt constraints; incentives, not regulation, are needed to induce more urban development.

The multifaceted nature of the crisis poses a deeper question: is London’s residential development model broken? Does it need to be rethought from the ground up?

London’s failing development model

London’s current development model has only really existed since the 2000s and relies on rising land values, high affordable housing quotas, and off-plan investor demand. This paper argues that this is now broken owing to economic, regulatory and market changes.

Private development has become unviable owing to increased costs, weaker demand and regulatory delays. Affordable housing faces similar problems; grants no longer make construction viable, Registered Providers are not taking on new stock, and in any case, provision in mixed-tenure schemes would be held back anyway by private sector issues.

The Government has introduced some welcome temporary measures aimed at kickstarting activity in London. These will be much more impactful than many in the market are assuming; while modest individually, acting together, they strongly support viability. There is still a need for a wider rethink of how London’s planning system delivers and regulates housing development if government targets are to be met in the longer term.

ten Recommendations for Policymakers

Our recommendations for the longer term include:

-

- Accelerate Gateway and planning processes.

- Relax the requirement for late-stage viability reviews.

- Reinstate Section 106BA reviews for viability reassessment.

- Offer relief from the Mayoral CIL as well as the local CIL.

- Extend recent measures to co-living and student accommodation to encourage more affordable housing delivery.

- Utilise public sector investment to unlock pension fund capital and accelerate plans for a National Housing Bank.

- Introduce some form of buyer support.

- Release low-quality green belt land for gentle density housing around stations.

- Further review design rules and space standards to permit higher density in Inner London, in particular.

- Update income ceilings for affordable housing access.

London Housing Model

Policymakers must recognise that in a world of higher interest rates, more attractive alternative investment options, and a weaker economy (at least in the short term), London property and land values can no longer be mined to the extent they were in the past, or expected to absorb the impacts of more costly and stringent regulation.

Attempts to do so will lead to even more stalled development in the future and a continued crisis in affordable housing provision, which in the capital is so linked. This is not just about viability; low land values will not incentivise owners to sell to developers, particularly in areas where alternative uses compete.

There will still be planning gain, which can justifiably be used for affordable housing and other social goods. But now and in the future, these may not be as large as in the past.

Instead, the new model must:

London’s Homebuilding Crisis: Working Towards a New Model for London Residential Development

6) Conclusions

The measures announced in September are a strong step in the right direction and together are much more effective than when considered in isolation.

But a combination of the recommendations above will also be needed to stimulate much-needed development in the longer term. and contribute to London’s economy and the well-being of its residents.

This raises the question of whether a deeper rethink is required. Private development at scale in much of London is a relatively new phenomenon. It has always been based on very different factors from most of the rest of the country.

These include:

- End prices that were assumed to be very high and constantly rising

- Investors (mostly but not exclusively overseas-based) buying off-plan, ‘unlocking’ finance for the development

- Support from Help-to-Buy in lower value locations (mostly Outer London), where investors were less active and affordability was less stretched

- Relatively strong demand from domestic owner-occupiers and, at times, from institutional investors (through build-to-rent)

- Very high land values (produced by the above) that could be used to provide large amounts of affordable housing and CIL revenue

In a world of higher interest rates, alternative investment options, and a weaker economy (at least in the short term), this model appears increasingly redundant. This rethink may require policymakers to think about how they can encourage and stimulate development in London, rather than how price increases can be used to support a growing list of wider objectives.

One of the overriding problems is that the post-war planning system was primarily designed with greenfield sites and new settlements in mind. The system we have for promoting and controlling urban development has been patched together according to a set of market conditions (and land supplies) that increasingly look historic.

Developers are unable to offer the prices that induce landowners, who are often in no rush to dispose of their long-term security, to sell. If residential land values fall below a certain point, other uses will become more appealing, or owners may simply opt to wait until conditions improve. This has huge ramifications for the supply of the raw material for development.

Aligning affordable housing so strongly with private development in London also means that it cannot act as a countercyclical stabiliser, helping to keep supply chains active and sites viable during market troughs (as appears to be happening in many other parts of the UK at present).

This paper does not argue that we should simply ignore planning gain. There will still be strong uplifts in land, created purely by planning consents, which can justifiably be used for affordable housing and other social goods. But now and in the future, these may not be as large as in the past, except in the most high-value areas.

In other words, we need a planning (and planning gain) system which:

London’s Homebuilding Crisis: What Needs to Happen?

5) Solutions

The Measures Announced So Far

The scale of the crisis has now been recognised by the government. On 23rd October, the Housing Secretary and the Mayor of London announced a package of policies aimed at kickstarting residential development. These include:

- A new ‘time-limited’ planning route – a ‘fast track’ – where developments on private land that commit to at least 20% affordable housing (of which 60% must be social rent) will not require viability testing. This figure will increase to 35% on public land or industrial land where the space is not re-provided. The measure will also apply to build-to-rent schemes where 30% of units are at London Living Rent.

- A 20% increase in the grant for social rented units.

- Temporary relief from Borough Community Infrastructure Levies (CILs).

- Removal of planning guidance maximising dual aspect units and constraining the number of units per floor.

These measures appear modest individually and have led to some disappointment in the market. However, our calculations show that acting together, they substantially increase viability, particularly for schemes in lower-value areas where deliverability has been weakest. Their impact should be substantial in the medium term.

However, a wider rethink of the housing model will be needed if London is in any hope of delivering in line with recent trends, let alone its targets.

It is also important to note, too, that none of the above measures apply to Purpose Built Student Accommodation (PBSA) and Co-Living – the two uses that are currently most viable in the capital, and have the greatest potential to deliver affordable housing in the short-term.

So, What Else Needs to Happen?

London is a very different housing market from the rest of the UK. Land values and end values are higher, but so are build costs; high-rise buildings and smaller flats account for a higher proportion of delivery; and affordable housing is expected to be delivered on a scale unmatched elsewhere in Britain.

Moreover, over the past few decades, London has accounted for a higher proportion of UK delivery than has been historically typical, making it far more critical to national housing goals – a situation that is not sustainable given market shifts and regulatory burdens.

Together, this means that London needs a different policy approach than the rest of the country, one that is essential if its contribution to overall national housing goals is to be reinstated. Our suggestions include:

- Accelerate the Gateway processes. This is absolutely critical, as this is the main source of delay in London. Resolving it might not lead to a huge jump in starts – given that other factors are dampening developer appetite – but it would support activity and mean more sites are ‘shovel ready’ when conditions improve. One potential option is to break the Gateway 2 processes down into phases, so that construction can start at an earlier point.

- Be even more flexible on affordable housing requirements. Ultimately, there needs to be a recognition that land values have fallen and can no longer sustain policies that were developed in different market conditions – and perhaps even an assumption that land values and prices can only rise. In short, the minimum requirements need to be cut back drastically, even if this is only temporary.

- Relax Requirement for Late-Stage Reviews. Late-Stage Reviews were introduced in 2017 to reassess viability and potential affordable housing contributions on schemes of 10 units or more after consent had been granted. This was successfully challenged in court, but still applied to larger developments that involved phases over several years or had delayed starts or completion dates. As this applies to many London schemes, it is a further risk and potential source of delay, disincentivising developers and funders. The measure was introduced at a time when the market was buoyant; given that this is no longer the case, the requirement should be relaxed.

- Reintroduce Section 106BA. Section 106 BA, BB and BC were introduced to the Town and Country Planning legislation in 2013. They allowed for a review of affordable housing requirements within five years of consent, based on viability. This was, to all intents and purposes, removed in 2016. Reinstating these clauses would seem sensible given the huge market shifts of the past few years. Encouraging and allowing such reviews could be key to making stalled sites viable.

- Reliefs to MCIL levies. The reliefs announced by the Government only apply to local authority CIL levies, but the high level of Mayoral CIL (MCIL) can be a major factor holding back development. Some form of temporary relief would help to make schemes more viable, particularly as MCIL is designed to increase in line with inflation even when pricing falls. It is understood that the MCIL is an important contribution to the funding of the Elizabeth Line, so this might have to be tied to future payments if and when the market recovers.

- Provide more support for build-to-rent. Policymakers have always been reluctant to back build-to-rent; they fear the electoral cost of not backing homeownership or in being seen to support corporate investment in people’s homes. But there is a huge appetite for the residential sector still among large-scale investors, and rental housing is important for a huge swathe of middle-income Londoners.. Applying less stringent affordable housing criteria to such developments, at least in the short term, would make the sector a more viable proposition for institutions. It is worth noting that the Government is keen to push local authority pension funds – including the London Pensions Fund Authority – to invest in housing and other forms of regeneration. This could be key to unlocking more housing sites in London.

- More public sector investment for affordable housing. Housing grant could be focused on schemes that are close to viability to enable both private and affordable housing delivery. But there are more radical approaches to unlocking capital, such as the use of public pension fund capital as set out above. This could be supported by the Government’s plans for a National Housing Bank, which need to be accelerated. The National Wealth Fund might be able to invest in affordable housing if it were reclassified as infrastructure. This funding could unlock private units as well if part of the same development.

- Introduce some form of buyer support. The end of Help to Buy has reduced the number of people able to access a mortgage, even if they can afford payments easily. However, it was a controversial policy, given the issues around valuation and risk. There are alternatives which could be more palatable, including reliefs on stamp duty or a modified Help-to-Buy requiring a larger buyer cash deposit.

- Release Low Quality Green Belt. Ultimately, the market is currently pushing away from high-rise urban development and towards more conventional housing. This needs to be catered for if housing delivery is to continue. This need not be unsustainable sprawl; there are huge opportunities to deliver ‘gentle density’ family housing (terraces, low-rise flats) on low-grade land around stations in the green belt. There are, fortunately, signs that the Government and the GLA are moving in this direction, not least in the designation of ‘grey belt’ – but this process needs to be accelerated.

- Allow more density in Inner London. While the market in Outer London is implying that more suburban development is demanded than planning permits, the reverse is true in Inner London, where there is the potential for greater height and smaller units, at least when activity recovers. Regulations could be relaxed beyond the measures recently announced. Such units often suit the younger, childless end-users, particularly in the rental sector, who are likely to spend relatively little time and home and do not envisage staying in the properties for longer than a few years.

- Apply new policy measures to Purpose Built Student Accommodation and CoLiving. The relaxation in affordable housing and viability tests should be applied to these tenures. As these uses are currently in high demand, they have the greatest potential to deliver units of all tenures – if given more flexibility. Furthermore, many local authorities have had ambivalent attitudes towards these uses, but they could offer even more in terms of delivery if given more encouragement.

- Update ceilings for accessing certain forms of affordable housing in line with London incomes. The ceiling household incomes of £67,000 for London Living Rent properties and £90,000 for Shared Ownership have not been updated since 2017. Between 2017 and 2024, median incomes in London rose by 29%. This alone suggests that the caps should now be circa £85,000 and £115,000 respectively.

London’s Homebuilding Crisis: Putting Things in Perspective

4) Perspective Taking

It’s important to bear in mind that large-scale private new-build development in London is a relatively recent phenomenon. According to a comprehensive database assembled by the think tank Centre for Cities, between 1955 and 1975, only around 200,000 homes were privately built in the capital, around three-quarters in Outer London boroughs, just 5.4% of the nation’s total.

To put this in context, this is slightly less than what was built in the eight-year period between 2016 and 2023 (when delivery was more evenly split between Inner and Outer London), when the capital accounted for 14.9% of private delivery.

This is, of course, private development. Social and affordable housing was a different matter. Between 1955 and 1975, London built some 300,000 affordable homes, half as many again as the private sector, or 12.4% of the UK total.

Inner London’s record is even more stark: 126,207 affordable homes and just 41,238 private homes.

Indeed, between 1974 and 1984, some 63% of all privately built London homes were delivered in just 10 boroughs: Bromley, Sutton, Barnet, Hillingdon, Bexley, Havering, Richmond, Enfield, Kingston and Harrow. Presumably, this reflects family housing on (relatively) greenfield sites.

Some London boroughs that are now deeply desirable saw extremely low delivery over that period – Tower Hamlets (just 316), Hammersmith & Fulham (just 369), Camden (just 442), and Lambeth (just 489). Hackney, Greenwich, Brent, Islington, and Wandsworth all saw fewer than 1,000 (or fewer than 100 homes per year).

This was not a period of any urban private housebuilding at scale. The industry largely built suburban homes and the odd medium-rise block of flats, while urban development was largely the province of councils. The exceptions were a few infill schemes carried out in the more affluent parts of London. In other words, there was no real at-scale urban private housing model. (The big regional cities were no different, incidentally, although many lacked infill projects too).

The following ten years – between 1985 and 1994 – were not so different. Inner London boroughs were delivering somewhat more (typically 500-1,250), but the likes of Hillingdon, Bromley, and Enfield remained the standout deliverers. There were two exceptions: Southwark and Tower Hamlets, which saw almost 10,000 and almost 6,000 private homes, respectively. This was a sign of what was to come, as it reflects the first large-scale private residential development in London since the likes of Dolphin Square before the war – the regeneration of Docklands and parts of the South Bank and Surrey Docks respectively.

The modern era of London development, though, can probably be dated back to the likes of the Montevetro scheme in Wandsworth, which was completed in 2000. It was the first large-scale luxury flatted development outside Docklands and would set the scene for a new wave of private development in London. By 1995-2015, the league table of delivery was led by Tower Hamlets and Southwark, with Westminster and Wandsworth high up in the table, a position that would continue: Inner London boroughs had become major contributors.

This was, of course, a reflection of changing attitudes towards Inner London – a so-called ‘gentrification’ that was being matched by a reversal in prices (Outer London boroughs were largely more expensive than inner ones in the decades after the war).

The history can be seen clearly in the chart below – London providing 14-18% of new builds post-war (a combination of reconstruction in Inner London and, more importantly, suburban expansion that had been approved before the modern planning system was introduced in 1947), followed by London making a 4-6% contribution to total private housebuilding in the sixties, seventies and eighties, mostly accounted for by Outer London (Inner London providing less than 2% for much of this period).

But as London’s renaissance kicked in, the figures for both rose, with Inner London in particular seeing private development of residential that had not occurred at anything like that scale for a very long time – arguably since late Victorian times.

The ‘broken model’ issue is more of a concern for Inner London. Of the 2,153 starts in London over the first six months of 2025, only 23% were in Inner London. This compares with a long-term trend of 39%. The boroughs seeing the highest number of starts in London were Barking & Dagenham, Barnet and Hounslow, where values are lower, development is less dense, easier and comprises low-rise flats or townhouses, and there is less affordability stress.

A further problem is that affordable housing delivery is now more linked to private development in a way that it was not the case in the immediate post-war period – partly because of section 106 agreements, partly because of the nature of development in London, with a majority of flatted, mixed-tenure blocks that cannot be built piecemeal.

In the mid-1970s, around 15% of affordable housing in the UK was being delivered in London; by the 2010s, this had risen to as much as a quarter. As a result of the general problems and the link with the viability of private schemes, it was probably around 2% over the year to the end of Q2 2025.

This leads to two important conclusions. Firstly, that London’s private sector has become far more important to national housing delivery. Secondly, as social housing has also become linked to that same private sector, it has become linked to market cycles and more vulnerable to downturns, like this one, that disproportionately impact private development in London. This implies that there is a need for a rethink of the whole system, rather than just some – admittedly helpful – emergency measures.