Market Pulse: Inflation Falls, Investment Rises and Key Sectors Begin to Recover

Download PDF

23 February, 2026 · 7 min read

Note: This briefing was finalised on 23 February, before recent events in Iran and the wider Middle East. Energy prices have spiked, and there are concerns that this could lead to higher inflation, slowing down the speed of future base rate cuts and, in turn, the speed of the gradual recovery outlined below. Much will depend on the length of the conflict and the resulting disruption to oil and gas supplies.

The final economic reading of the year, GDP growth in Q4, came in with a lacklustre 0.1%, but over 2025, the UK economy grew by 1.3%. This is clearly not spectacular, but it is not terrible either – which might come as a surprise given the economic doom and gloom in the press. Even GDP per capita rose by 1.0% over the year, up from a big fat zero in 2024.

This kind of story is repeated across lots of datasets in both property markets and the wider economy. Slowly, things are beginning to improve, albeit usually at an unimpressive rate. But the results should be more apparent as 2026 progresses.

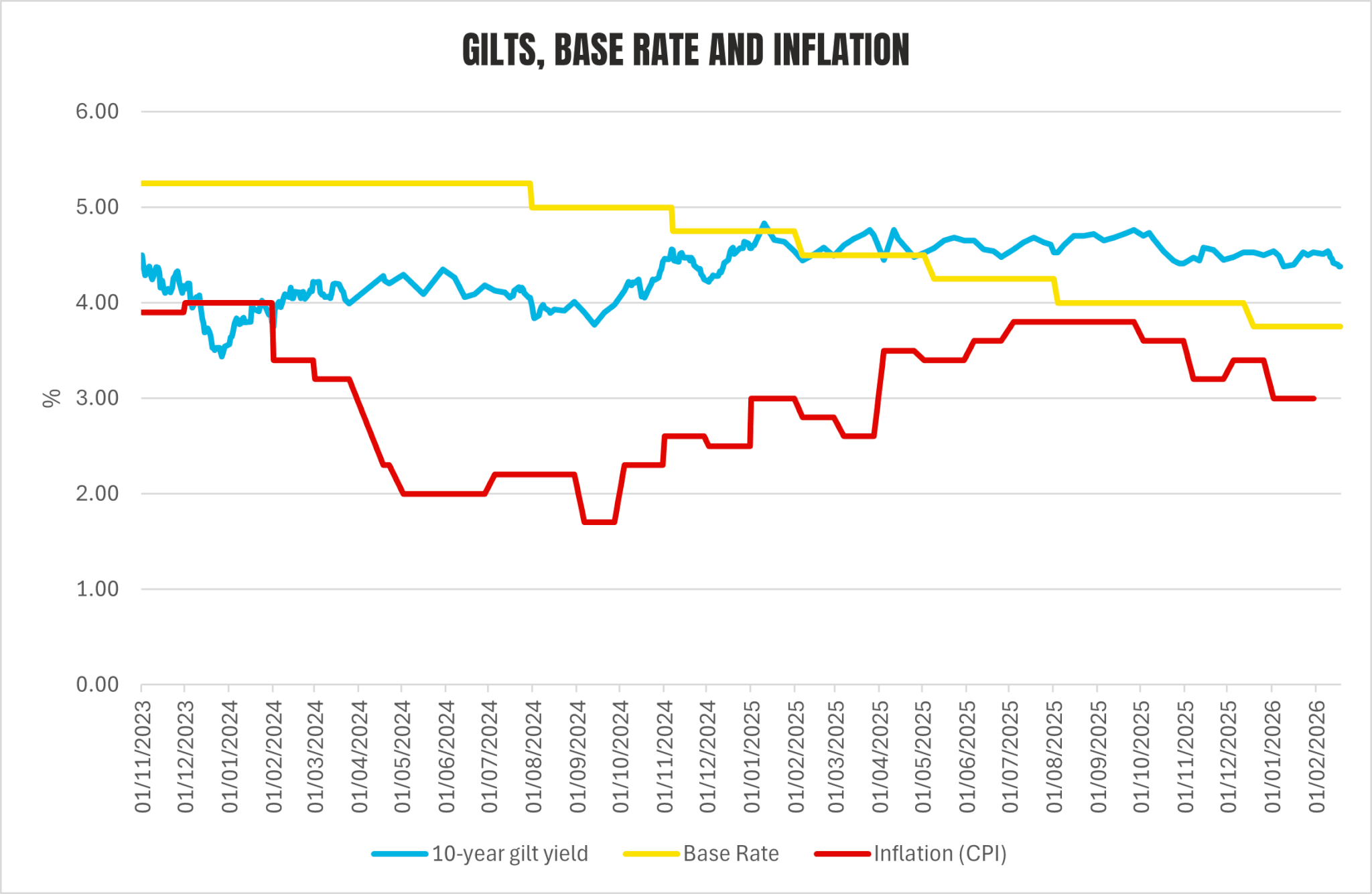

Take inflation as measured by CPI. December’s outturn was a little disappointing – 3.4%, up from 3.2% in November and slightly ahead of market expectations. But January saw it fall to 3.0%. Since the Summer peak, the trend has been clearly downwards. This is evident in the labour market, which is becoming looser; redundancies are increasing, vacancies are decreasing, and private sector wage growth is slowing.

The Bank of England had adopted a slow and cautious approach to cuts, with forecasters expecting just another two 25bps cuts over 2026, bringing the base rate to 3.25% by year-end. But it’s entirely possible that if all these measures continue trending downwards, there is another 25bps by year-end.

The slightly better economy is, of course, related to falling inflation and interest rates as well as the surprising fact that business investment has been running at historic highs since the pandemic (presumably related to technology). Oxford Economics is forecasting a slightly gloomier GDP growth of just 0.9% in 2026, but this may well be overshot if the wider context continues improving.

10-year gilts, the ‘risk-free rate’ against which property returns are compared, are a slightly different story. The bond market is not only reacting somewhat slower to changes – reflecting the scale of government borrowing both domestically and internationally – it is more volatile. This reflects the UK’s fragility, not just its own poor finances but also the vulnerable position of Kier Starmer and Rachel Reeves. Their replacement with a less fiscally conservative pairing is clearly a risk. At the time of writing, there are also rumours – indications, even – of further ‘events’ in the Middle East, which would also upset the wider picture.

Source: Bank of England + National Statistics + Market Watch

Assuming that none of this derails things too much, then bond yields should follow their choppy path downwards, with the result that property yields gradually become more appealing. Indeed, there is some evidence that the combination of solid if uninspiring growth, reducing rates and strengthening fundamentals in some markets has already been enough to get the market moving again.

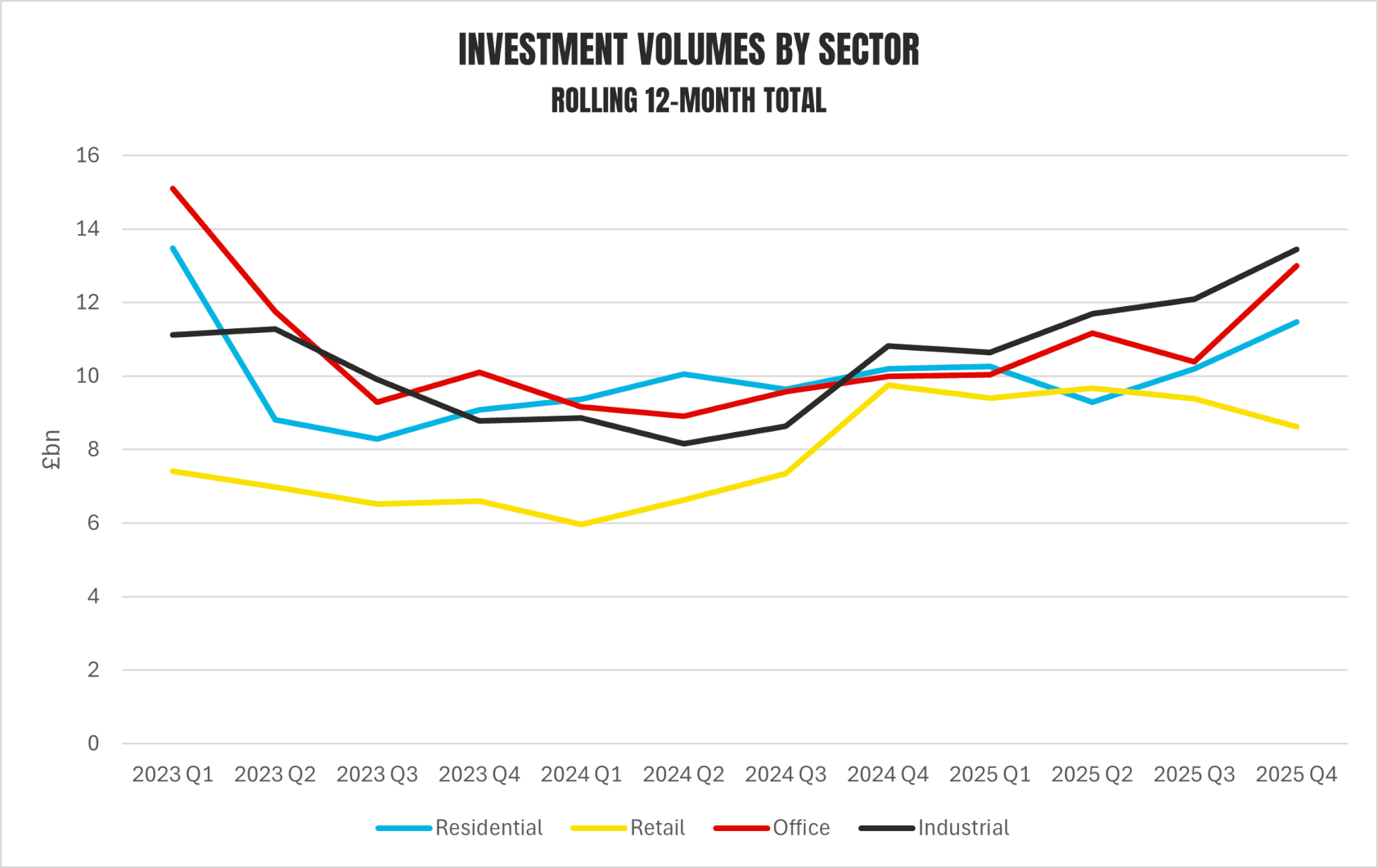

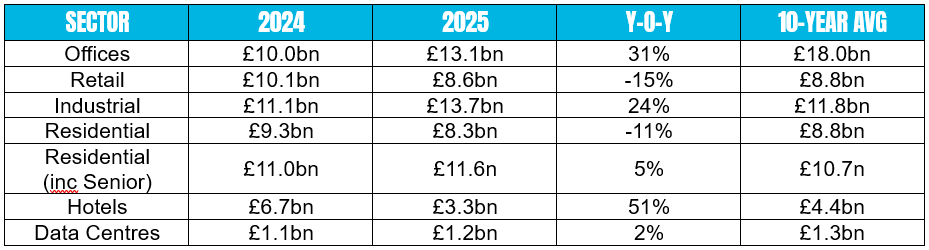

The final quarter of the year saw £17.1bn transacted, the highest total for almost four years. As can be seen below, every sector except retail is now seeing a steady upward trend. The standout was undoubtedly offices, which, with £6bn changing hands, saw the highest total since 2021. This was driven by some large-scale deals in London, with some major international institutions (Hines, Royal London) re-entering the fray.

Source: MSCI

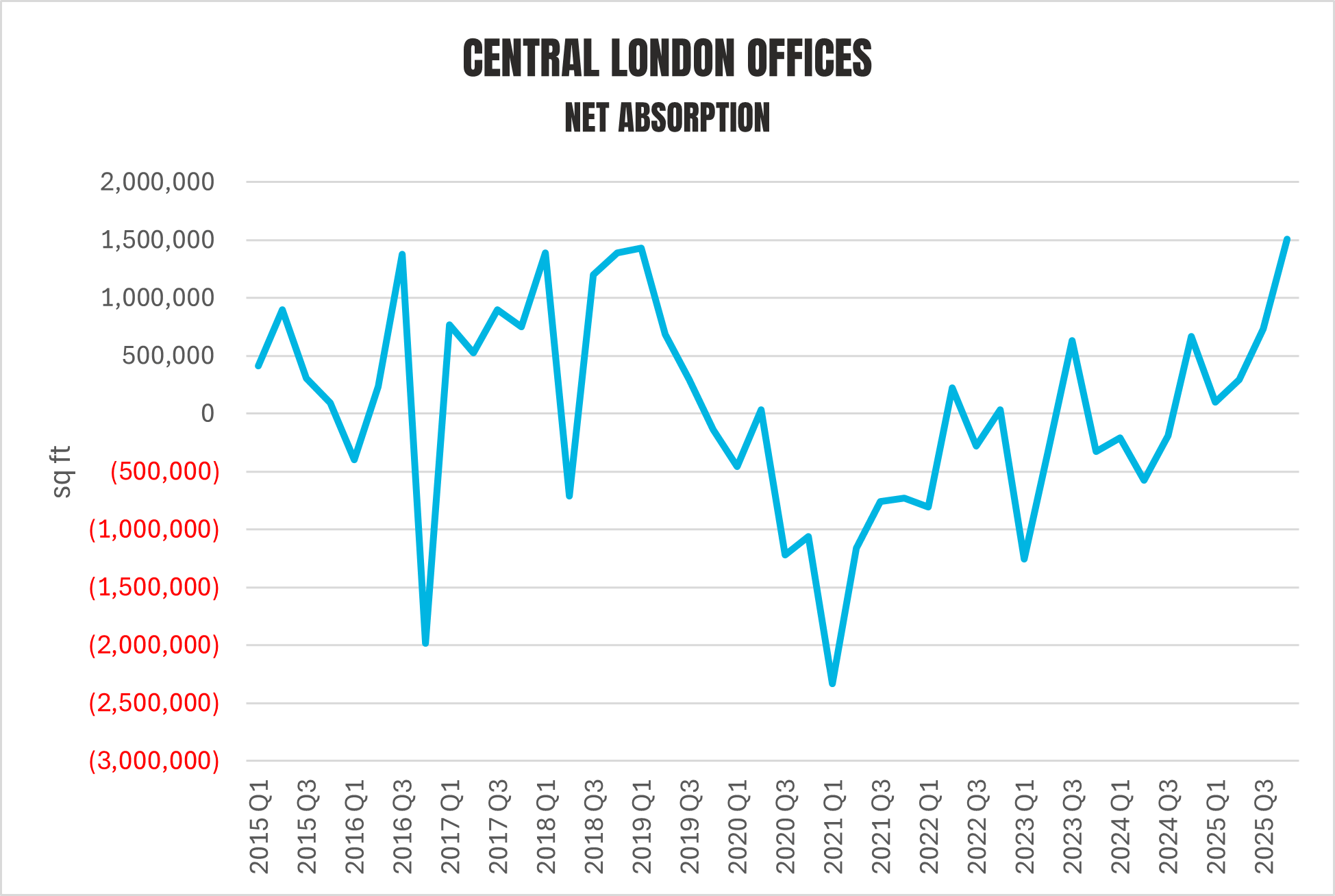

The strong fundamentals in London’s office market have been apparent for a while. Rental growth has been strong, with prime city rents now at circa £100psf, compared to say £75psf three years ago. High vacancy rates obscure the shortage of new, high-quality offices that occupiers increasingly crave. Prelets have increased as businesses have looked to the pipeline, rather than the increasingly obsolescent-looking existing stock.

Net absorption in the Central London market was at its highest on record, even though leasing fell back, suggesting that companies are simply becoming less minded to leave space given constrained availability. Meanwhile, space under construction and construction starts are lower than they were a year ago. But most importantly, investor sentiment has turned, and even if you are sceptical about the arguments around polarisation, the herding effect alone should see both values and volumes rise over 2026.

Source: CoStar

The situation is, if anything, even more stark in the major cities outside London. There have been practically zero starts in every ‘big six’ city except one, and vanishingly small amounts under construction. Manchester stands out as the exception, with 400,000 sq ft started over the past twelve months. It is true that this city had the highest take-up over 2025, but it is not so far ahead of the pack to justify such an incongruity. I do wonder if some of the recent hype over its economy is skewing investment. Now that’s not to say it is doing well – it very clearly is, as any time spent in the city will confirm – but there are some questions over whether the very high figures for productivity growth (see here) are accurate.

Industrial, on the other hand, is still seeing very strong investment, albeit not the great jump upwards seen by offices. The total for 2025, at £11.1bn, was the highest of any sector (just), and represented a 24% increase on 2024. I’ve had mild concerns about industrial for a while; leasing has been muted for two years or so, while vacancy has been rising, and rental growth has slowed considerably.

But over the last few months, a corner has been turned. The pattern is similar to the London office market – falling vacancy and increasing net absorption amid lower leasing activity. This implies that companies are simply not moving because there is insufficient new, good-quality space. (The main difference, though, is that the standout region now is the North-West).

Source: MSCI

So, in offices, residential and industrial, in some locations at least, the market is effectively screaming ‘build’. But that is more easily said than done. Construction costs and development debt costs remain high. Moreover, yields have not yet really budged downwards, partly a result of what’s happening in the gilt market.

The increase in investor interest should push yields down over the next year, at least in the London office market and at least by 25bps. The resulting increase in exit price will begin to make construction more viable, but in the medium term, the situation looks set to be one of shortage and increasing prices, assuming demand remains robust. This will continue to push rents for good-quality stock upwards, further supporting viability. This will take time to fix, though, meaning the whole issue of refurbishment and ‘retrofix’ moves up the agenda again as demand returns.

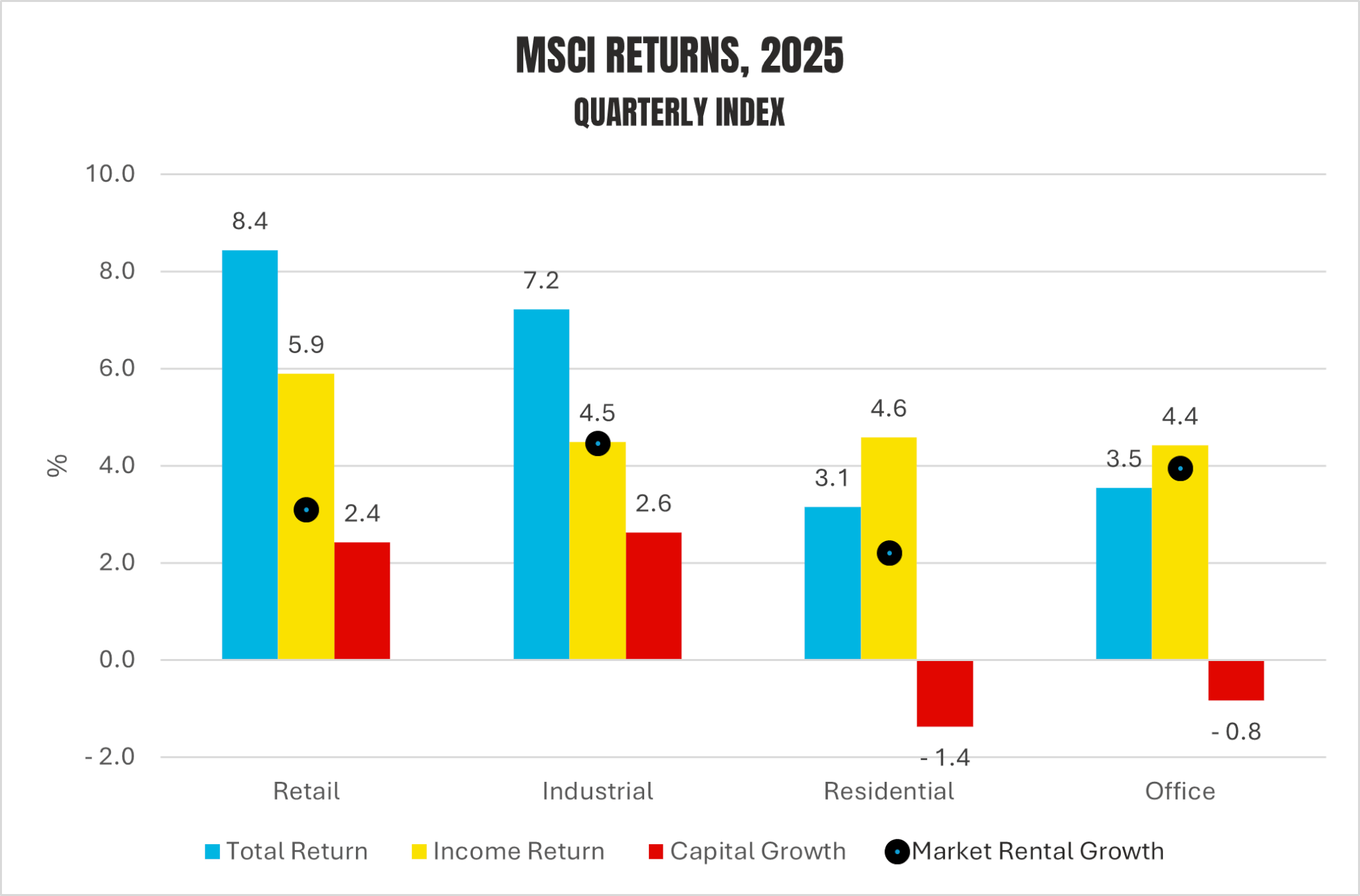

Looking at the MSCI performance data, though, retail saw the strongest returns in 2025 – 8.4%, driven mainly by very strong income returns (5.9%). As outlined above, retail spending is buoyant, and the flatness in internet sales proportions has confirmed that bricks-and-mortar shops have a future. The sector is now seeing rental and capital value growth, too – although all from the low base produced by the long years in the wilderness.

Source: MSCI

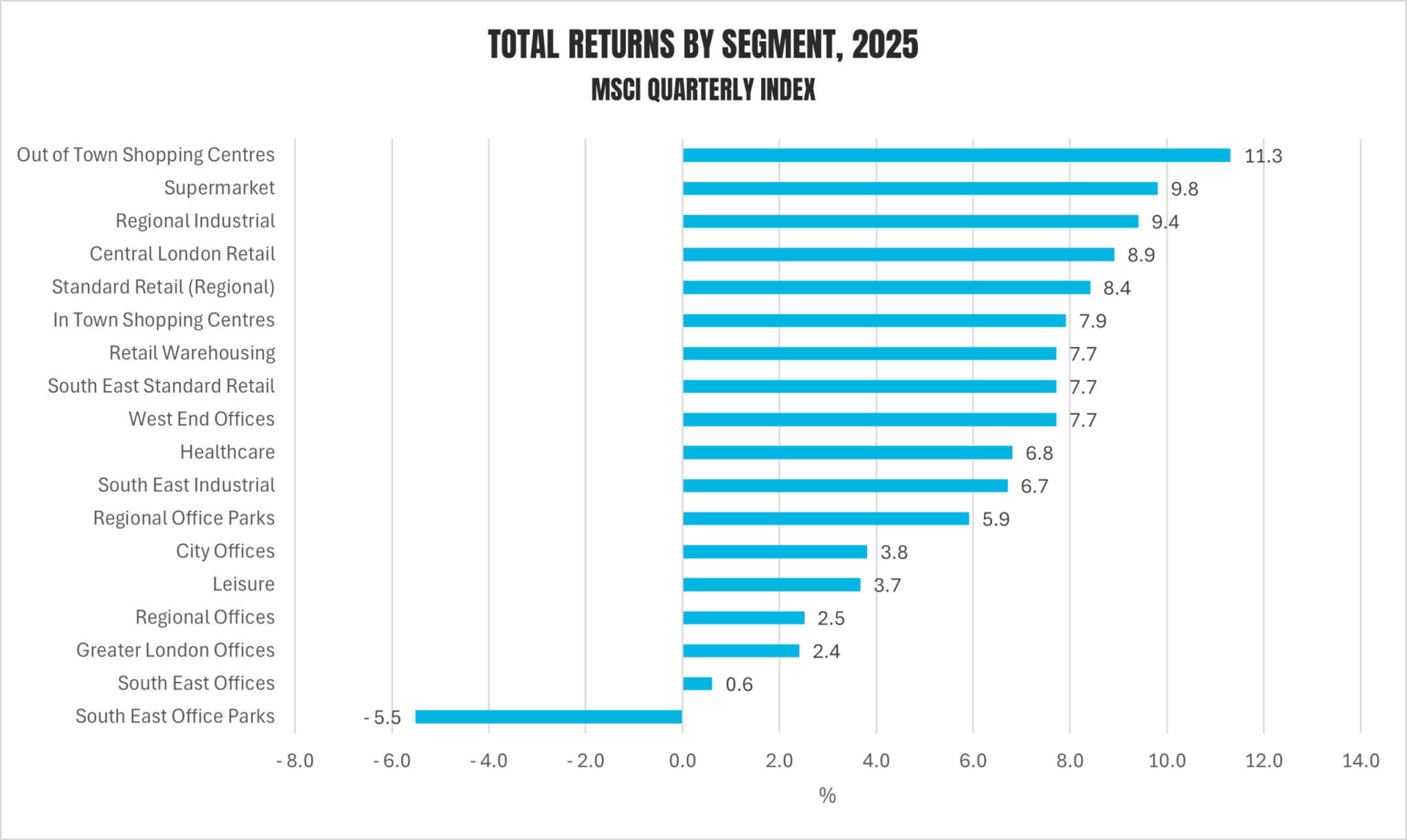

Of course, retail warehousing, supermarkets and out-of-town shopping centres have been doing well for a while, but the difference now is that they are joined by standard regional retail (8.4%) and Central London retail (8.9%). The weakness in investment may be more to do with a lack of supply, with investors perhaps choosing to hold onto such strongly income-producing stock.

Offices, on the other hand, remain highly polarised with West End offices’ total returns at 7.7%, and South East office parks at -5.5%. The urbanisation of office demand, particularly in the South, continues.

Source: MSCI

Source: MSCI

Despite weak returns, residential is still seeing high volumes, though a number of large senior living transactions in Q4 skew the figures slightly; activity in the BTR sector slowed slightly towards the end of the year. However, there has been a resurgence in interest from investors, with a flurry of deals in London. At the end of 2025, M&G announced a joint venture with NPS, the Korean pension fund, to invest up to £1bn in UK multifamily, and other funds are gearing up for action. Meanwhile, Notting Hill Genesis’s sale of its BTR arm is also attracting huge interest.

This reflects gradually improving conditions in the London residential sector (see our research here) alongside the huge long-term potential of the sector, given low construction, rising population and persistent housing undersupply.

Conditions in the residential market are no exception to the slow improvement rule. Mortgage rates for higher LTVs have come down by almost a percentage point over the past year, and look set to fall further; greater competition for borrowers will force down margins even as rates fall. The rental market will become increasingly constrained over the year as the supply of properties falls back, a result of the combination of recent low BTR activity and smaller-scale landlords continuing to exit the market.

At the moment, though, the North and Midlands look more buoyant in terms of pricing and activity across both sides of the market, a result, really, of housing taking up a smaller proportion of people’s pay. But the above factors will lead to a recovery in London, where affordability has been most challenged.

So, in summary, wherever we look, the market seems to have reached an inflexion point. Unless something dramatic happens, things should get better in most sectors from now on. Just don’t expect a boom, though.

If you have any questions about this briefing note or any other aspect of the commercial or residential market, please contact jon.neale@montagu-evans.co.uk. We also carry out bespoke research for clients to inform strategy, guide policy or aid in individual sites or developments.

*This research has been prepared for general information purposes only. It does not constitute any investment, financial or other specialised advice or recommendations, and you should not, therefore, rely on its contents for such purposes. You should seek separate professional advice if required.

Download PDF